Artificial‑intelligence servers have rapidly become one of the most important growth engines for tantalum polymer capacitors.

As this demand accelerates, according to the industry sources and customer notes, tantalum capacitor manufacturers have implemented a series of price adjustments to reflect tighter capacity utilization and higher raw‑material costs, while the broader tantalum supply chain moves into an investment and optimization cycle rather than a crisis phase.

Key Takeaways

- AI server tantalum capacitors drive rising demand, prompting KEMET to implement price adjustments for the third time in under a year.

- The price hikes reflect structural changes due to increased usage of tantalum capacitors in AI servers and data centers, tightening availability but maintaining an orderly market.

- Tantalum raw-material prices have surged, driven by capacitor demand and disruptions in Central Africa, yet appear managed rather than chaotic.

- Long-term investment in tantalum production supports future availability, as the market adapts to high-reliability demands in the AI era.

- Manufacturers are optimizing designs and sourcing strategies, ensuring supply chain resilience while addressing the growing need for AI server components.

According to recent market reports, KEMET YAGEO group will raise tantalum capacitor prices for the third time in less than 12 months, with the latest increase reported to become effective on April 1. Earlier rounds of adjustments in 2025 already lifted prices for selected tantalum polymer series, typically in the 20–30% range for certain voltage and capacitance combinations. These steps have focused on high‑demand product families used in AI servers, data‑center hardware, and networking infrastructure, where design wins and shipment volumes are growing the fastest.

Instead of a sudden shock, the pattern resembles a phased repricing process in tantalum capacitor manufacturers. This process involves re-aligning contracts and list prices with the new demand environment and increased upstream costs. From a purchasing perspective, customers will notice multiple incremental adjustments over several quarters instead of a single disruptive jump. This allows engineering and sourcing teams to adapt designs, forecasts, and negotiations accordingly.

AI servers as a structural demand driver

The catalyst behind these moves is a structural shift in end‑market demand, led by the rapid deployment of AI servers and accelerator platforms in hyperscale data centers. Compared with traditional enterprise servers, AI systems typically integrate more high‑current power rails, tighter transient requirements, and higher power densities, all of which favor robust, low‑ESR decoupling components such as polymer tantalum capacitors in critical power‑management stages.

As cloud providers scale out AI training and inference clusters, the number of tantalum capacitors per rack and per server has risen, and design wins for polymer Ta in AI power trees have become strategically important for leading suppliers. This has tightened available capacity for certain case sizes and voltage/capacitance ranges, especially in popular 2.5–10 V segments at mid‑to‑high capacitance values. Importantly, this shift looks like a multi‑year adoption curve rather than a short‑term spike, as AI workloads become embedded in cloud, edge, and enterprise architectures.

A tight but orderly tantalum capacitor market

From the customer perspective, the immediate impact is visible in higher unit prices and, in some cases, extended lead times for selected tantalum capacitor series. Market trackers describe the environment as tight, with allocation in certain niches, but still orderly rather than chaotic or disrupted. Buyers who forecast and communicate demand early generally retain access to supply, while spot or last‑minute needs can face steeper pricing and longer delivery times.

Upstream, tantalum raw‑material prices have firmed as capacitor‑grade demand has strengthened and some Central African supply has been disrupted. Recent assessments show tantalum concentrate prices up more than 40% year‑to‑date and tantalum metal in Europe up around 60% over the same period, driven by a combination of capacitor demand and mining issues in the Democratic Republic of Congo and Rwanda. Even with this strong move, the market still functions, with material available to contracted buyers and no broad evidence of production stoppages at major capacitor makers.

This picture is consistent with the longer‑term trends documented in the Passive Component Raw Material Price Index, which shows that tantalum prices had actually eased into 2023–24 before their latest rebound, and that volatility has been a recurring characteristic of capacitor‑grade metals over the past several years.

Long‑term tantalum trends: high prices, resilient supply

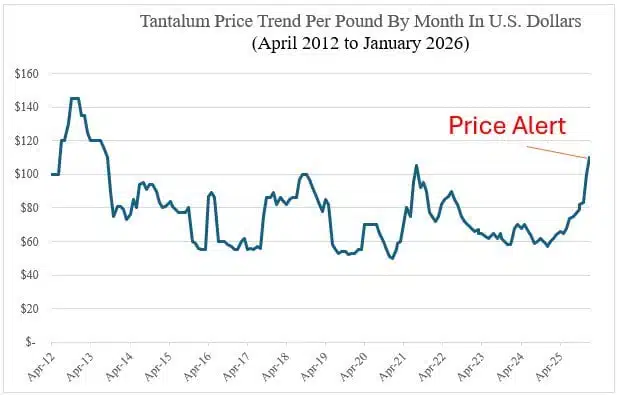

Recent analysis of 165 months of tantalum ore pricing confirms that today’s elevated raw‑material costs are part of a long‑running volatility cycle rather than a sudden shock specific to AI demand[9]. Prices peaked around 145 USD per pound in 2012 during the conflict‑minerals transition, then corrected to roughly 55 USD per pound by 2016 as compliance stabilized, Australian production ramped and inventories were digested across the supply chain. After several years of relative stability in the 55–85 USD range, the market went through pandemic‑era swings and a new structural rally from mid‑2024, with ore now around 115 USD per pound—more than 100% above 2024 lows.

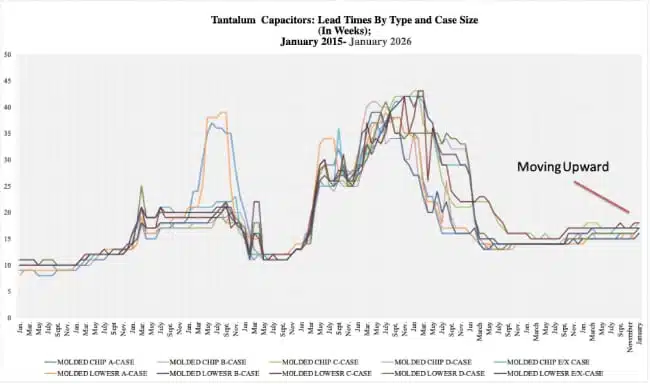

Despite this strong ore move, tantalum capacitor lead times have remained in a manageable 16–18‑week band, well below the 35–43‑week peaks seen in past shortage periods. Continuous tracking of 132 months of lead‑time data shows that manufacturers are still shipping reliably and absorbing much of the cost increase, which supports AI, automotive and industrial programs without the disruption seen in earlier cycles. The data suggests a gradually tightening but resilient supply chain where structural demand growth from AI and EVs is being met by disciplined capacity management rather than panic expansion or abrupt allocation.

From a design and purchasing perspective, this history reinforces the positive, long‑term view of tantalum capacitors in AI infrastructure. The technology has already weathered conflict‑mineral legislation, pandemic logistics shocks and multiple demand inflection points while remaining a preferred solution for high‑reliability power delivery. As AI data‑center deployment accelerates, the combination of proven supply‑chain resilience, stable lead times and strong vendor commitment indicates that tantalum capacitors are well positioned to support the next wave of AI server growth—provided customers continue to plan ahead and secure strategic agreements.

How tantalum prices trends compare to other passive‑component metals

While tantalum has seen one of the sharpest recent price moves among metals relevant to passive components, it is not the only material experiencing volatility. Industry tracking of passive‑component raw materials shows that copper, silver, and ruthenium remain elevated versus pre‑pandemic levels, while aluminum, nickel, and zinc had largely stabilized by late 2024 and palladium and tantalum had previously eased before their latest rebound.

| Metal | Recent trend (2024–early 2026) | Key drivers for passive components |

|---|---|---|

| Tantalum | Strong rise in 2025–26; concentrate up ~40%+ YTD, metal in Europe up ~60% YTD. | AI and electronics capacitor demand; supply risks in DRC/Rwanda. |

| Silver | At multi‑year highs, supported by broad precious‑metal rally and strong investor interest. | Thick‑film pastes, terminations; higher prices flow into resistor and MLCC costs. |

| Copper | Elevated vs. pre‑2020; benefited from industrial‑metal up‑cycle and energy‑transition demand. | Leadframes, foils, wiring; broad cost baseline for many passive parts. |

| Nickel | Volatile but largely stabilized by late 2024, with some weakness versus earlier peaks. | Certain alloys, terminations; less extreme recent move than tantalum. |

| Palladium | Came down substantially into 2024 after previous peaks; still sensitive to auto‑catalyst trends. | MLCC electrodes (legacy designs) and some specialty applications. |

| Ruthenium | Prices remained elevated vs. pre‑pandemic; moderate upward movement in 2024–25 after earlier softness. | Thick‑film resistor pastes, especially high‑value precision resistors. |

For capacitor and resistor manufacturers, this mix means that tantalum is currently one of the more aggressively repriced inputs, but it is part of a wider context in which several key raw materials remain structurally more expensive than in the late 2010s. That backdrop helps explain why downstream component pricing has moved upward across multiple technologies, not just tantalum capacitors, even though the AI‑server story is currently most visible in the market narrative.

Supporting investment and long‑term availability

One constructive way to interpret the recent tantalum capacitor price moves is as enablers of future capacity rather than pure cost increases. Higher selling prices for critical product lines improve the return on investment for new tantalum capacitor production equipment, process upgrades, and quality‑assurance capabilities. In a segment where qualification cycles can be long and reliability requirements are stringent, securing stable margins is a prerequisite for sustained, long‑term supply to high‑reliability and data‑center customers.

At the same time, the industry is not standing still on the demand side. System and power‑design engineers are actively optimizing AI server platforms, balancing MLCCs, polymer Ta, and other technologies to achieve the best combination of electrical performance, reliability, and cost. By refining derating strategies, case‑size selections, and parallel configurations, OEMs can use tantalum capacity more efficiently while maintaining or improving system robustness. This co‑optimization between component suppliers and end‑system designers is a key mechanism that helps prevent localized tightness from turning into a broader supply‑chain problem.

Outlook: investment and optimization cycle

Looking ahead, the tantalum capacitor market appears to be entering an investment and optimization cycle rather than a crisis phase. Strong AI‑server demand, combined with growth in automotive and industrial electronics, is likely to keep the market firm, but current signals still point to a tight‑yet‑manageable environment for well‑planned programs. Additional capacity investments by major players, supported by the recent series of price adjustments, should gradually expand available supply and improve flexibility over the coming years.

For purchasing and engineering teams, the key responses are strategic rather than reactive: early forecasting, close communication with suppliers, and thoughtful design choices around capacitor technologies and derating can significantly reduce risk. For the industry as a whole, the latest move is best read as another sign that tantalum capacitors remain deeply relevant in the AI era – and that the supply chain is actively adapting to support that role over the long term.

References

- Yageo subsidiary Kemet hikes tantalum capacitor prices for third time as strong AI server demand continues – DigiTimes

https://www.digitimes.com/news/a20260302PD239/yageo-tantalum-capacitor-price-increase-ai-server-demand.html - KEMET raises tantalum capacitor prices as AI demand tightens supply – SemiMedia

https://www.semimedia.cc/20284.html - Tantalum Capacitor Rally on AI: Panasonic Reportedly Hikes 15–30%, Yageo Rides Wave – TrendForce

https://www.trendforce.com/news/2025/11/28/news-tantalum-capacitor-rally-on-ai-panasonic-reportedly-hikes-15-30-yageo-rides-wave - Ta prices surge on capacitor demand, tight supply – Argus Media

https://www.argusmedia.com/en/news-and-insights/latest-market-news/2791031-ta-prices-surge-on-capacitor-demand-tight-supply - Tantalum Prices Rise in 2025 as Critical Mineral Demand Intensifies – IMARC Group

https://www.imarcgroup.com/news/tantalum-price-trend - Passive Component Raw Material Price Index Stabilizes in September 2024 – Passive Components Blog / EPCI

https://passive-components.eu/passive-component-raw-material-price-index-stabilizes-in-september-2024/ - Passive Component Raw Material Index Increases in Q1 2025 – Passive Components Blog

https://passive-components.eu/passive-component-raw-material-index-increases-in-q1-2025/ - How Metal Prices Are Driving Passive Component Price Hikes – Passive Components Blog

https://passive-components.eu/how-metal-prices-are-driving-passive-component-price-hikes/ - The Tantalum Paradox: Rising Ore Prices Meet Resilient Supply Chains – Paumanok, TTI MarketEYE

https://www.tti.com/content/ttiinc/en/resources/marketeye/categories/passives/me-zogbi-20260211.html