ECIA’s Electronic Component Sales Trend Sentiment (ECST) survey continue to surge upward in April 2024.

The latest results from ECIA’s ECST survey show optimism continuing to surge upward in its measurement of overall sales sentiment for April and May among electronic components supply chain players.

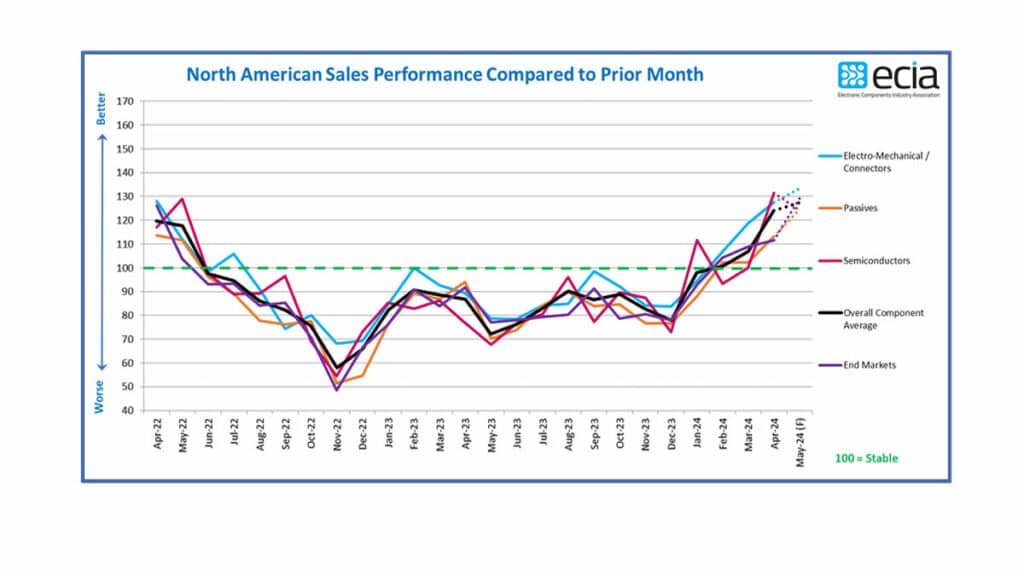

The ECST overall index score jumped up by 17.2 points between March and April to reach 124.1. The outlook for May shows continued improvement as the overall index moves up to 127.4 which would be the highest score since February 2022. In a stunning leap, Semiconductors saw their index score soar upward by over 31 points to top 131.

Passive components and Electro-Mechanical components both saw impressive upward improvement as well increasing their index scores by 11 and 9 points,

respectively. As a result, the sales sentiment for all three categories delivers highly positive results with scores ranging between 113 and 131. Expectations looking toward May reveal sustained upward momentum in sentiment as Passive and Electro-Mechanical components continue to climb upward reaching 133.4 and 124.6, respectively.

Semiconductors fall back slightly from their April high but still come in at 124.2. The ECST survey results point to a strong start for Electronics Component sales in the first half of 2024 with consistent, month-to-month improvement for five months following a low of 77.8 in December.

The April survey results show continued consistency among all three groups in the survey: Distributors, Manufacturers, and Manufacturer Representatives. It is notable the Manufacturer Representatives have continued to align with the other groups following a pattern of much more conservative scores up to February of 2024. In fact, in a surprising development, Manufacturer Representatives deliver the strongest scores looking toward May. Again, this broad-based optimism among all three groups strengthens confidence in the survey results.

Interestingly, the index score for end markets improves only slightly in April. However, it then jumps ahead of the component score in the May outlook as it tops 129. The forecast that every market segment but one would top 100 in April was realized. The score for Automotive has stagnated at around 98 for four months now.

Avionics/Military/Space, Medical, and Industrial Electronics continue to be the strong drivers of positive sentiment in the end-market index. All three registered scores above 120 in April. The outlook for May anticipates Automotive achieving strong improvement with a score surpassing 120. The market segment with the lowest May outlook is Telecom Mobile Phones at 108.3.

The markets all continue to face strong headwinds in the form of slower economic growth, inflation, and uncertainty of future actions congress and the Federal Reserve. Hopefully, the sales sentiment for markets and products will drive revenue growth despite the current challenging environment.

The strong renewed demand for DRAM and Flash memory has resulted in a jump in reports of increasing lead times in these product areas. This is reflected in the increase in overall Semiconductor upward lead time pressure. Passive Components and Electro-Mechanical Components show slight upward pressure in lead times but are still dominated by reports of stability.

Overall, the reports of declining lead times have shrunk to 6% while increasing lead time reports grew to 10%. The net outcome is an increase of stable lead time reports from 81% to 83%. While there are continued concerns in many areas of the electronic components supply chain, especially excess inventory, the metrics measured by the Electronic Components Sales Trend (ECST) survey portray an industry in a very healthy state.