ECIA’s Electronic Component Sales Trend Sentiment (ECST) survey participants in December 2023 looking with confidence toward January 2024.

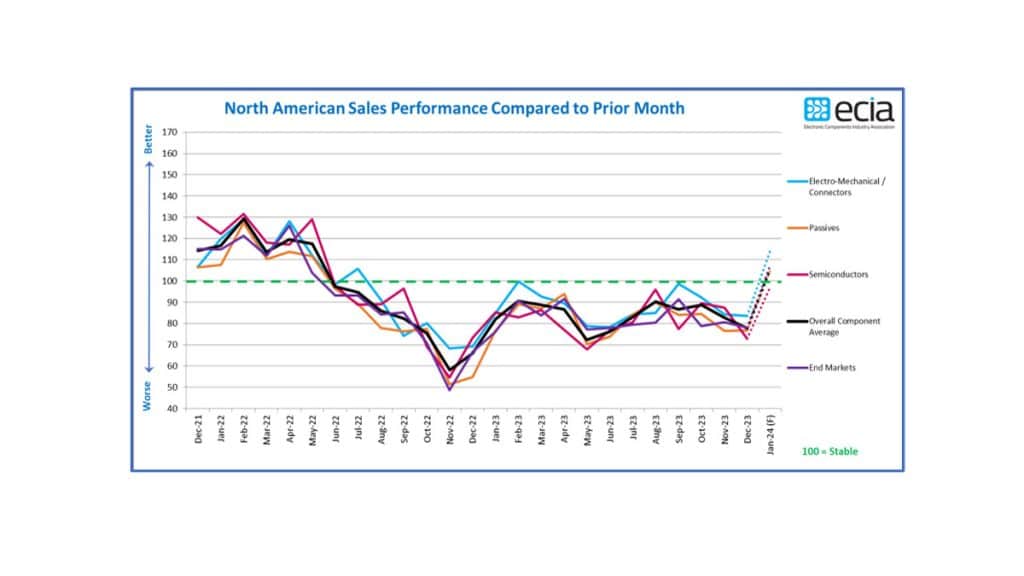

Following a year of overall index scores languishing between 72.2 and 90.6, respondents to the December Electronic Component Sales Trend (ECST) survey are suddenly and strikingly optimistic in their expectations for January 2024.

The actual sentiment index result for December came in at 77.8, 5.5 points below the already modest outlook of 83.3 for December as reported in the November survey. For the full year of 2023, none of the major component segments achieved an index score at or above 100 which would have indicated positive sales growth sentiment. Expectations for January have shot up by 27.8 points in the overall index to hit an average of 105.6 points.

If this projected growth is actually realized in January, it would be the strongest month-to-month growth in the history of the index with the exception of one month in June 2020. As always, some caution in expectations is prudent given previous disappointments in index results falling below expectations. However, this is a highly encouraging sign to start 2024.

The Electro-Mechanical / Connector category came close to topping the 100-point threshold level two times in the past year. It now registers the highest score in the January outlook at 114.4, a 30.7-point jump from December. This is followed by the Passive components category with a 28.4-point jump driving it up to 105.2 in the January projection. Despite its leap of 24.4 points, the Semiconductor category falls short of passing the 100-point mark as it comes in at 97.4 in the January forecast.

During 2023, the projection for overall growth in the index in the coming month fell far short of lofty expectations at least three times. All three of the major categories were expected to top 100-points at some point during the year only to fall short. Hence the need to sound a note of caution for the January 2024 outlook. Despite this concern, even if the index achieves half of the forecast improvement in January, it will represent an extremely healthy start to the year.

Following an established pattern, manufacturer representatives presented the lowest expectations for January. However, even this group projects an improvement of over 25 points between December and January. The expected improvement reported by Distributors and Manufacturers was only marginally better than manufacturer representatives at 29.3 and 27.9 points. This base of strong expectations across all three of the major reporting segments serves to boost confidence in the overall outlook. The strong January forecast improvement across all three major component categories is also encouraging.

The overall end-market index follows the same trend as the component indices with a forecast January leap of 29.5 index points. Every end-market segment is forecast to see major improvements in their scores with Industrial Electronics expected to achieve the biggest improvement of over 36 index points.

The highest overall forecast index score for January is reported for Avionics/Military/Industrial at 136 points. The lowest expectation is for Consumer Electronics at 88 points. However, the Consumer Electronics outlook for January is higher than all but two of the actual scores for end-market segments in December. To summarize, the Electronics Components industry enters the new year with remarkably high expectations.