The European electronic components distribution market delivered a robust return to growth in the first quarter of 2026, but DMASS Europe warns that this momentum still rests on a fragile macroeconomic and geopolitical foundation.

Solid double‑digit growth across Europe

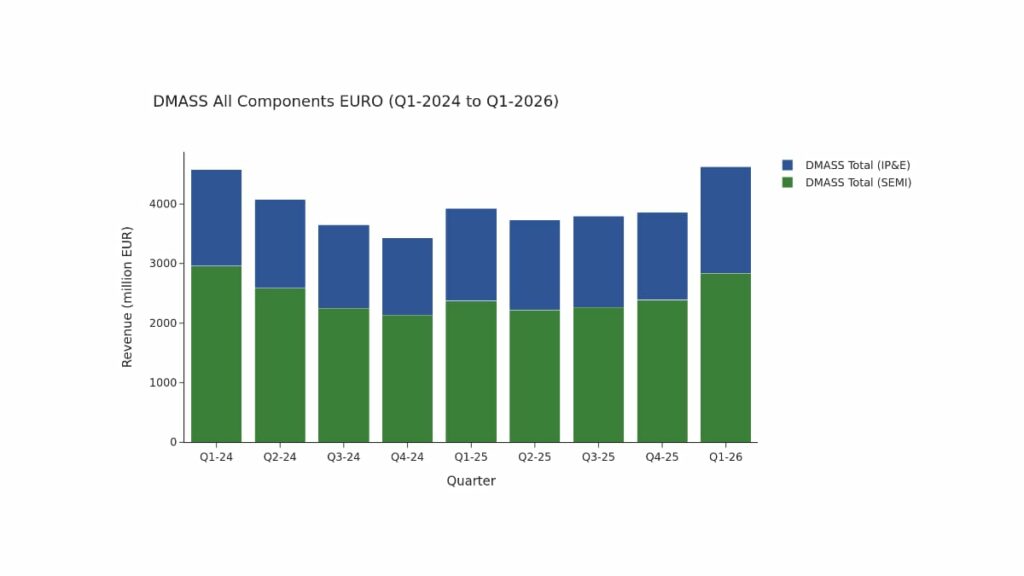

European components distribution revenue climbed to €4.63 billion in Q1 2026, an increase of 16.9% year‑on‑year. Semiconductor distribution reached €2.84 billion with growth of 18.2%, while interconnect, passive and electromechanical components (IP&E) advanced to €1.79 billion, up 14.8%.

Core industrial economies such as Germany, Italy, the Nordics, Austria and Benelux all posted strong double‑digit gains, confirming that industrial demand remains the backbone of the European components market. Turkey stood out with exceptional growth close to 40%, underlining its rising importance as a regional logistics and trading hub, while Ireland and parts of Southern Europe expanded more cautiously.

Russia remains effectively absent from the DMASS statistics, with sanctions continuing to halt formal electronic component distribution into the market. Overall, the regional pattern is heterogeneous, with growth driven by industrial and automation projects rather than the consumer and hyperscale‑AI booms seen in the US and Asia.

| Country/Region All Comps. | Total € | Change Q1/Q1 |

|---|---|---|

| UK | 384.237 | 10,1% |

| IRELAND | 39.254 | 4,6% |

| GERMANY | 1.079.423 | 18,5% |

| FRANCE | 397.094 | 12,5% |

| ITALY | 481.537 | 18,8% |

| SWITZERLAND | 155.512 | 12,1% |

| NORDIC | 403.914 | 19,8% |

| BENELUX | 185.899 | 21,0% |

| IBERIA | 269.124 | 15,1% |

| AUSTRIA | 99.911 | 22,4% |

| RUSSIA | 0 | 0 |

| EASTERN EUROPE | 816.758 | 17,9% |

| ISRAEL | 141.847 | 8,1% |

| TURKEY | 113.592 | 37,9% |

| OTHER | 63.596 | 13,4% |

| DMASS All Comps. Total | 4.631.700 | 16,9% |

Memory‑driven semiconductor upswing

On the semiconductor side, the Q1 picture is dominated by an exceptional rebound in memory products, which posted triple‑digit year‑on‑year growth and have become the single most dynamic segment in European distribution. High‑bandwidth memory for data‑center and AI workloads is absorbing large parts of global capacity, leading to tightening availability and upward price pressure that are now clearly visible at the distribution level.

Discrete devices and sensors and actuators continued to grow at solid double‑digit rates, reflecting healthy demand across industrial automation, power conversion and sensing applications. Analog and power semiconductors showed a more measured recovery in the low‑to‑mid double‑digit range, closely tied to the pace of projects in automotive, energy and factory automation.

Programmable logic and standard logic remained under pressure, with negative growth as customers continue to digest inventories and delay new design‑ins in some segments.

This divergence underlines how strongly the current cycle is skewed toward memory‑intensive AI and data‑center deployments, while more traditional segments move at a slower but steadier pace.

IP&E components: broad but uneven recovery

The IP&E segment mirrored the overall market upturn, reaching €1.79 billion in Q1 and expanding by 14.8% year‑on‑year.

Eastern Europe, the Nordics, Ireland, Switzerland and Iberia delivered the strongest percentage gains, while Germany, Italy and Benelux contributed solid volume growth that reflects their large installed industrial base. The UK and France continued to grow, albeit at mid‑single‑digit to high‑single‑digit rates, pointing to more cautious investment behaviour in some customer segments. Turkey again stood out with very high double‑digit expansion, benefiting from its role as a bridge between European demand and supply flows from Asia and the Middle East.

| Country/Region IP&E | Total k€ | Change Q1/Q1 |

|---|---|---|

| UK | 183.349 | 7,5% |

| IRELAND | 14.621 | 19,3% |

| GERMANY | 365.116 | 14,7% |

| FRANCE | 174.400 | 6,8% |

| ITALY | 191.424 | 13,1% |

| SWITZERLAND | 47.142 | 17,9% |

| NORDIC | 163.228 | 18,2% |

| BENELUX | 84.822 | 12,1% |

| IBERIA | 117.158 | 17,6% |

| AUSTRIA | 40.483 | 13,5% |

| RUSSIA | 0 | 0 |

| EASTERN EUROPE | 286.665 | 22,1% |

| ISRAEL | 45.329 | 10,7% |

| TURKEY | 51.651 | 35,0% |

| OTHER | 27.566 | 11,5% |

| DMASS IP&E Total | 1.792.956 | 14,8% |

Within IP&E, passive components recorded revenue of around €634 million with growth around the mid‑teens, supported by stabilising lead times and renewed pull‑in from industrial customers. Electromechanical components exceeded €1 billion in sales and grew at a similar rate, helped by investments in automation, infrastructure and energy‑related projects across the region.

| Product Group IP&E | Total k€ | Change Q1/Q1 |

|---|---|---|

| PASSIVES | 633.571 | 16,0% |

| ELECTROMECHANIC | 1.032.029 | 14,9% |

| POWER SUPPLIES | 127.356 | 8,6% |

| DMASS IP&E Total | 1.792.956 | 14,8% |

Structural risks and AI gap keep foundation fragile

DMASS Europe points to a clear improvement in the demand environment compared to the downturn of 2024, but emphasises that the new growth phase is still exposed to multiple external risks. Geopolitical tensions, energy‑price volatility and fragile logistics chains remain key concerns for European distributors and their customers.

Unlike the US and parts of Asia, where hyperscale cloud and AI data‑center build‑outs are a dominant driver, Europe’s demand profile remains heavily weighted toward industrial applications, automation and automotive. This gives the European market a steadier, more application‑driven character, but also means that it is more vulnerable to industrial slowdowns and external shocks in global trade and energy supply.

According to DMASS, the task for the industry is to convert the current rebound into more resilient, long‑term growth by improving supply‑chain robustness, reducing structural dependencies and strengthening Europe’s position in strategic technology domains. Key priorities include securing access to critical semiconductor and passive component capacity, managing allocation in memory and other constrained product groups, and deepening application support to help customers navigate volatile market conditions.

About DMASS Europe

DMASS Europe e.V. is the only industry body that collects detailed quarterly distribution data for electronic components in Europe, covering both semiconductors and IP&E across a wide range of product families. The organisation represents close to 90% of the European distribution total available market, providing its members with a granular statistical tool to benchmark performance by country and by product group. Founded in 1989, DMASS has grown into a pan‑European platform with several dozen distributor and manufacturer members, including leading global semiconductor, passive component and interconnect suppliers. By publishing consolidated quarterly figures, DMASS supports greater transparency for the electronics ecosystem and offers a reference point for assessing business cycles and regional dynamics.

Source

This article is based on information and figures provided by DMASS Europe e.V. in its official Q1 2026 European Components Distribution press release.

References