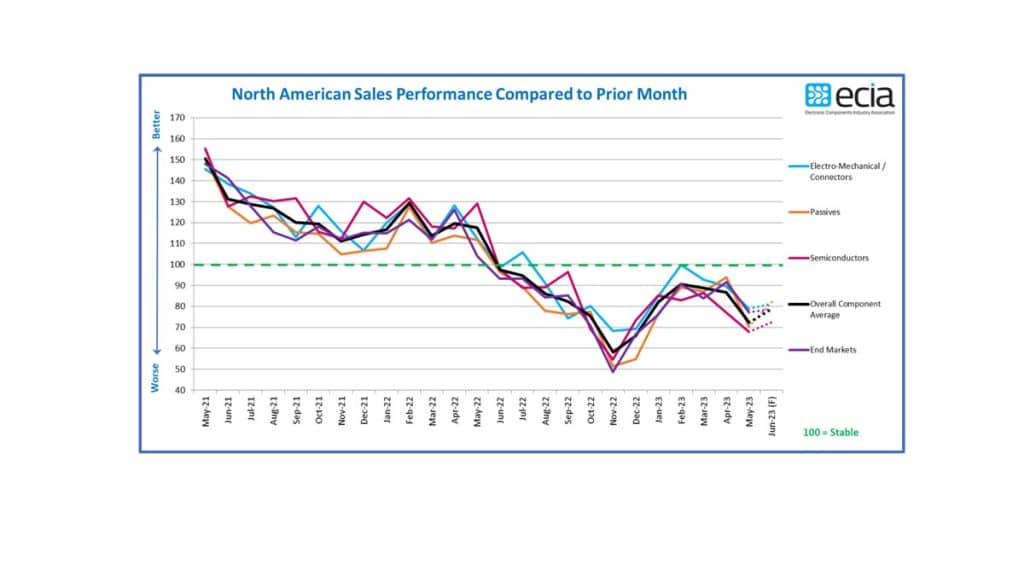

The May ECST survey results reported by ECIA show overall sales sentiment took a body blow compared to expectations and collapsed to 72.2 points compared to expectations for May from the previous survey of 99.1 points.

The May index fell by 14.5 points compared to the April index of 86.8. This is the third month in a row of declining results. The June outlook only improves modestly to 78.6 points. The most recent ECST results are a dramatic reversal from expectations of sales sentiment achieving an overall positive outlook over 100 in May.

The results of the May survey combined with the Q2 ECST survey results point to an extended market recovery period with a turnaround in year-over-year growth coming at the end of 2023 at the earliest.

The sales sentiment of Manufacturers compared to Distributors and Manufacturer Representatives reveals very different views of the market. Distributors and Manufacturer Representatives delivered extremely bearish inputs with overall index scores of 71 and 60 respectively. At the same time, the overall Manufacturer average registered at 91 with three component categories scoring at or above 100.

A review of the survey results reveals that this divergent view of the world started in April. One possible explanation for these extremely different views could be that Manufacturers are seeing stronger performance in their direct business while inventory balancing in the distribution channel is still in process.

While Semiconductors scored the lowest in the overall May index, Passive Components experienced the steepest month-to-month fall in the index as they collapsed by nearly 24 points. While the Electro-Mechanical / Connectors sales sentiment index delivered the best result for May it is not a source of optimism.

The overall end-market trends reflect the same downward slide as reported in the product index. The Avionics/Military/Space sentiment is the only market that did not see a sharp increase in negative sentiment in May. This segment continues to reflect a high level of optimism.

In a distant second place, the Automotive market achieved a rough balance between better sales expectations compared to worse expectations in both the current month and the June outlook. Every other segment, including, surprisingly, Automotive Electronics, is in deep red sales sentiment territory.

The results reported in the Quarterly ECST survey indicate that a return to meaningful Quarter-toQuarter growth will have to wait until Q4 at the earliest. Sentiment reported for the current Q2 quarter and the Q3 outlook is dominated by flat sales expectations in both quarters. Those expecting declining sales are slightly higher than positive sales expectations in Q2. That is reversed in Q3 as overall positive growth expectations come in at 32%, above the 28% with negative expectations.

A summary analysis of the ECST results from May and Q2 points to continued downward sales pressure through the first half of the year with the possibility of achieving equilibrium in Q3 ahead of renewed growth hopefully in Q4 or Q1.

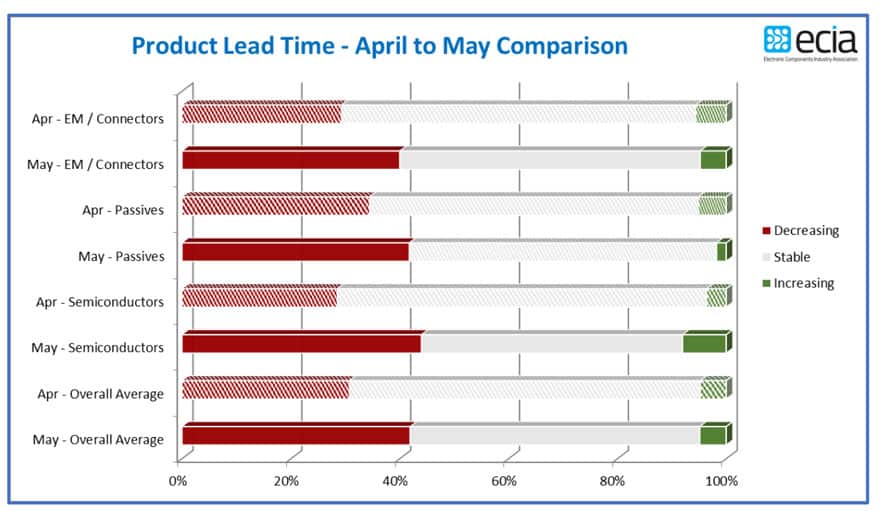

Product lead time trends in the latest ECST survey show a continuing level of “stability” with growing levels of decreasing lead times. 53% of survey respondents saw Semiconductor lead times as stable, down from 64% in April. This decline in stable lead times was matched by a jump in decreasing lead times from 31% to 42%. Increasing lead times reports remain at a negligible 5% level.

As noted before, credit for the improving lead time picture does need to be given to increased production. Given the overall assessment that inventory overhang is the greatest challenge facing the supply chain currently, product mix issues would appear to be the main contributor to any reports of increasing lead times as inventories balance out in the declining market.