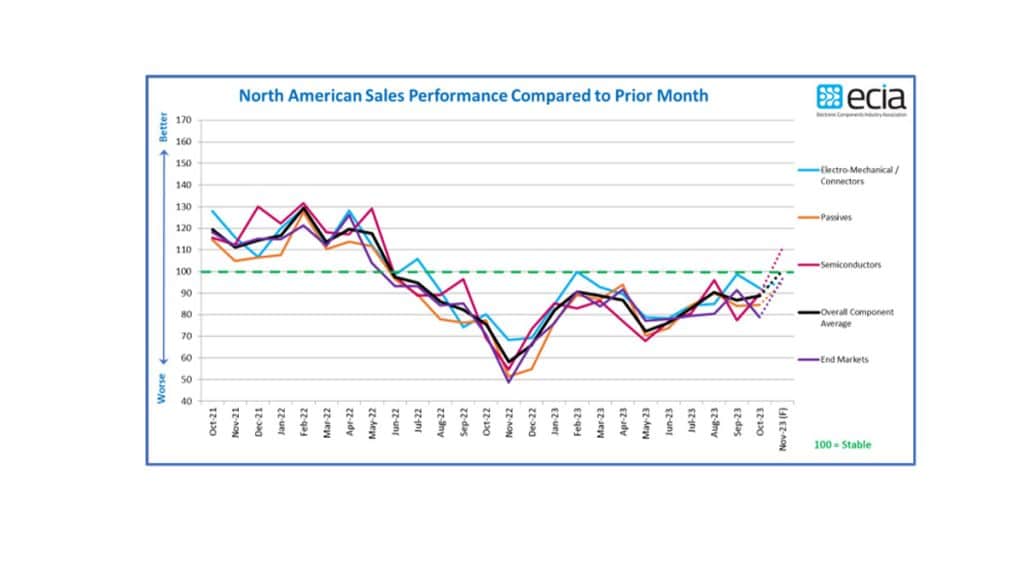

ECIA’s Electronic Component Sales Trend Sentiment (ECST) for October 2023 sales sentiment survey underperformed expectations in October.

The July, August, and September surveys pointed to overall component sales sentiment scoring between 94.0 and 94.8 in the coming month.

The actual results came in between 86.7 and 90.3. On average, sales sentiment results scored 5.9 points below expectations in August, September, and October.

The good news is that the October sales sentiment score improved over September by 2.1 points reaching 88.8. But this is still far short of the 100-point threshold indicating positive growth in month-to-month sales. Despite historical disappointment, the survey points to a major November improvement that would push the overall component score above 100. Leading the way is the semiconductor category with a November outlook of 111.1. The major semiconductor subcategories are more conservative in their average outlook as they come in at 99.3.

The optimism for November is broad based with the Passive and Electro-Mechanical categories outlooks come in at 95.0 and 95.1 respectively. Almost as optimistic as the semiconductor forecast for improvement, the overall

end-market score leaps by 18.1 points to reach 96.9 in November.

If the combined outlook for all major segments is realized in November it would be the strongest result since June 2022. The electronic components industry continues to stand on the brink of passing the breakeven point by the end of the year with the potential for return to broad-based growth at the beginning of 2024.

The chasm in sales sentiment between manufacturer representatives and manufacturers and distributors widened dramatically in the October survey. A major disconnect began in April and widened in June and July before narrowing somewhat in August and September. The average sentiment scores from Manufacturing Representatives plummeted by nearly 10 points between September and October. At the same time, overall scores from Distributors and Manufacturers remained relatively stable monthto-month.

A stark difference in perspectives persists across the supply chain. The index scores from Distributors range between 87 and 118 for the major categories in October. By contrast, the manufacturer representative scores range between 38 and 75, an overall drop of 10 points from the prior month. The Manufacturer scores only dropped by around 2 points from September to October. As they stand on the front lines in the supply chain, Manufacturer Representatives appear to see a much more challenging sales environment than their partners in the supply chain.

The overall end-market index lost all of its September gains as it fell by 12.6 points back to 78.8 in October. This is a strong departure from the product index trends in October. However, the end-market index also projects a strong November rebound with a jump of 18.1 points to 96.9. Industrial Electronics is the most volatile segment in the end markets as it experienced a strong drop to 84.4 in October but projects a jump to 100.0 in November. Avionics/Military/Space continues to outpace all other market segments while Mobile Phones struggle at the bottom of the pack. Every end market category projects strong November improvement except Medical Electronics with a minor slip and a flattish outlook for Automotive Electronics and Avionics/Military/Space.

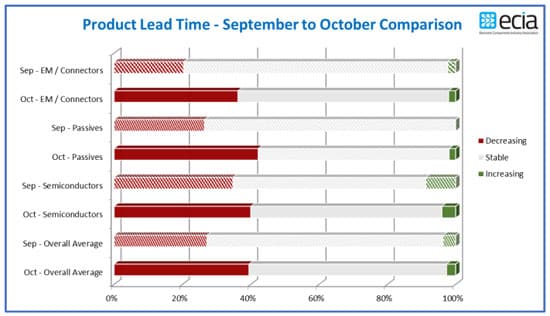

The picture for product lead time trends has settled into an extremely healthy view. Stable lead times continue to dominate the responses with stable average lead times holding steady at 69% in October responses. Increasing average lead time reports were at an inconsequential level between 2% and 4% in October. Resistors, NAND Flash Memory, MPUs, and MCUs had zero reports for increasing lead times. Yet again, the lead time results provide some of the most positive outcomes in the ECST survey.