Edgewater Research’s IP&E report suggests that the momentum for recovery is continuing to build and strengthen. However, the roadmaps for AI platforms remain in flux. Nevertheless, the overall outlook for AI remains positive.

This April 2026 collection of news summaries, survey results, and channel market insights, covers Interconnect, Passives, and Electromechanical Components from Edgewater Research.

What’s Changed/What’s New?

- First-quarter demand is projected to surpass targets, with B2B and non-automotive sectors accelerating to a 1.25-1.35x growth rate compared to the 1.1x growth rate expected at the beginning of the year. The visibility and backlog have improved compared to 90 days ago, which supports the above-seasonal 2Q sales trends and a double-digit outlook for the year.

- Nvidia Kyber officially still targets a 2H27 ramp, although the supply chain sees an increasing probability of a delay to 2H28 (Feynman) due to signal integrity performance tied to Nvidia’s midplane based on the POGO-Pin connector design.

- If Kyber is delayed, Rubin Ultra is likely to leverage the Oberon NVL72x2 rack design, with copper backplane intra-rack and copper or optics for rack-to-rack connections.

- TE is expected to exit the first quarter with a lower-than-expected 30% share on the GB300 cable backplane due to a slower ramp and more limited Nvidia tooling and engineering support.

Top 3 Channel Comments:

- First-quarter shipments exceeded our expectations, with Q/Q sales growth of 10% above plan. Bookings were even stronger, with B2B sales exceeding 1.3x. We observed a broad-based recovery in distribution POS, with particular strength in the industrial sector. The 2Q outlook is projected to increase by 7-8% Q/Q, which is conservative given that we already have 100% firm orders in hand, and this does not factor in price increases.

- We believe Nvidia was convinced by its component partners that the Kyber midplane technology is not ready for MP, at least not for now. Rubin Ultra’s timeline. POGO Pins connectors are a challenging technology. The major connector suppliers haven’t been able to deploy them in MP for high-speed applications, only in testing. The biggest challenges are vibrations and signal integrity.

- Some programs are targeting optical scale-up architectures for the 2028+ timeframe. However, the key gating factor remains backend integration at TSMC, particularly packaging, assembly, and test. Until that ecosystem is proven at scale, deployments are likely to be limited to early design-ins rather than broad volume adoption.

Other Key Takeaways:

- 1Q AI/DC connector demand is expected to see a significant increase, with a double-digit Q/Q organic growth rate (>100% Y/Y). The 2Q outlook is also expected to be positive, with another double-digit growth rate. The industry transition to optics is still viewed as phased into the 28/29 timeframe. Enterprise inference buildout is gaining momentum into 2027, driving additional TAM.

- POGO-Pins connectors are considered unproven at scale for high-speed use due to their high cost and signal integrity limitations. Nvidia is targeting to qualify five or more suppliers, but it’s unclear how many of them could meet the volume and quality specifications. Amphenol is developing HD Paladin 3 connectors as a backup.

- The FIT HD Paladin ramp at Nvidia is projected for 2027, mainly supporting inference racks with a limited 10-15% share on compute racks.

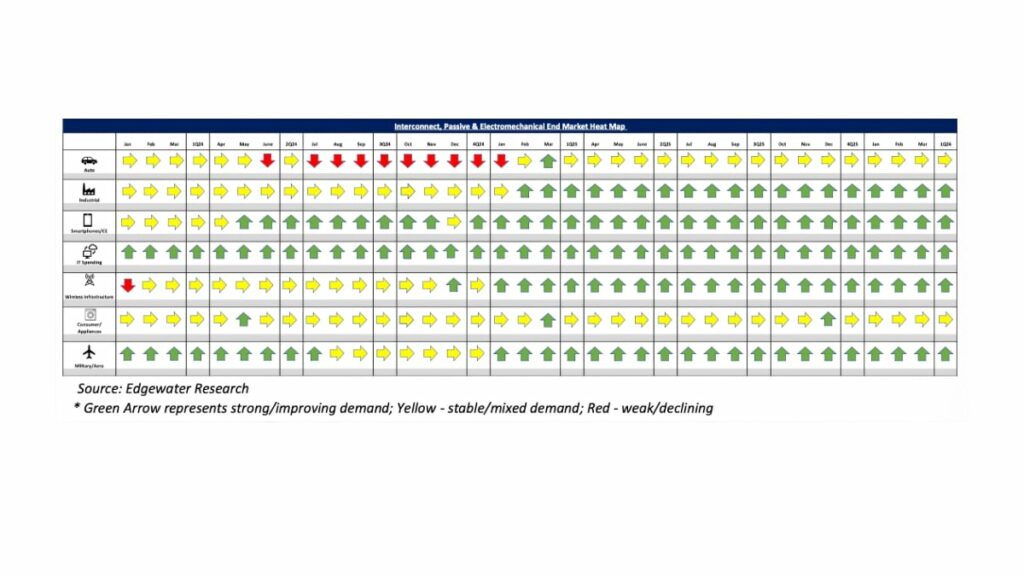

- The auto demand is expected to be resilient, in line with the better-than-feared outlook in 1Q. The CY26 outlook remains unchanged at an up to low to mid single-digit percentage.

- Comm Transportation is still muted, with limited signs of recovery in the West and moderate improvement in China.

- Industrial inflecting broadly in 1Q, with B2B and backlogs supporting upward revisions in outlooks and messaging.

- Connector pricing is still upward trending, with incremental channel actions expected by May or July due to rising resin costs.

- Passives and electromechanically shipments and bookings are expected to show positive growth in 1Q, with broad-based strength across categories driven by strength in Industrial/distribution and AI/DC. MLCC and resistors lead times are expected to extend the most in 1Q, and pricing is also expected to increase.

Conclusion:

IP&E fundamentals are improving significantly, particularly in the M/M segment. There’s broad-based strength in bookings, pricing momentum, and end demand, and there’s no sign of slowing in the AI buildout. While the auto market is lagging behind other markets, it has remained resilient and outperformed expectations.

With supply chain momentum continuing and visibility improving, we remain optimistic about the fundamentals through the balance of 2026 and into early 2027. However, we’re keeping an eye out for any signs of pull-forward driven by pricing or any demand impact from memory. Absent these risks, the fundamentals should remain healthy and continue to support growth across the IP&E industry into 2027.

Full report available from: Dennis Reed, Sr. Research Analyst, Edgewater Research