Sales confidence in the electronic components industry surged in March 2026, with the latest ECIA Industry Pulse survey reporting the highest overall sales sentiment index in five years, reaching 149.2, a level not seen since April 2021.

This strong result underscores a broad-based improvement in demand across components and end markets, extending the positive momentum that has been building since mid‑2025.

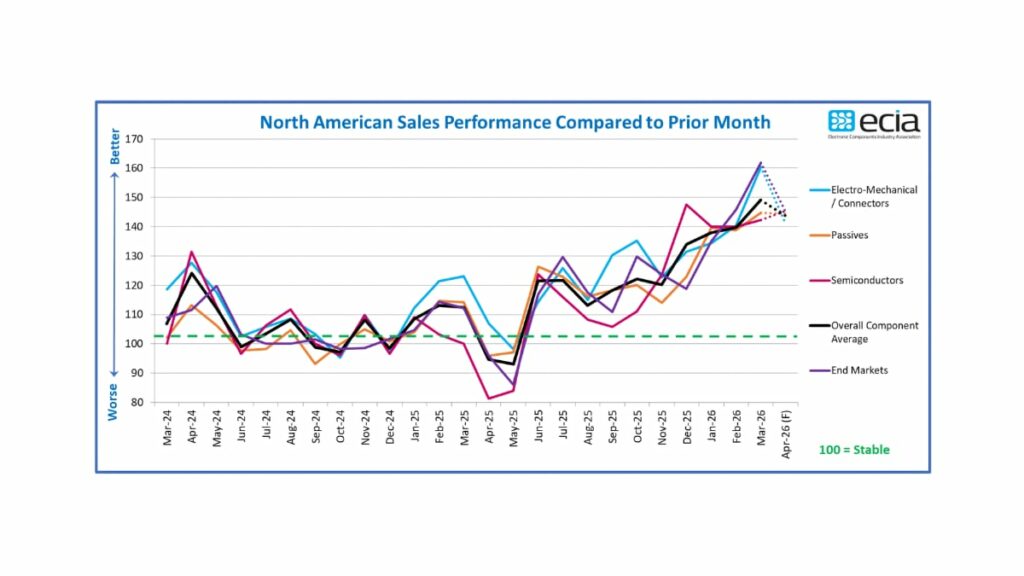

Broad-Based Strength Across All Major Component Categories

The March survey shows that all three major component categories—Semiconductors, Passives, and Electro-Mechanical/Connectors—recorded solid month-on-month gains in sentiment.

- Electro-Mechanical/Connectors led the upswing with a jump of more than 20 index points, marking the strongest improvement among all categories.

- Semiconductors and Passives also posted robust increases, maintaining firmly positive readings well above the 100-point threshold that separates expansion from contraction in the ECIA index.

This synchronized improvement across component categories indicates that the current upturn is not limited to a single technology segment, but reflects a broad, structural recovery in electronic component demand.

End-Market Sentiment Reaches New Peak

On the demand side, end-market sentiment moved in lockstep with the component categories.

- The overall end-market index climbed by more than 16 points in March to approximately 162, signaling very strong demand expectations across customer segments.

- Historically strong segments such as Avionics/Military/Space and Industrial continue to deliver some of the highest sentiment scores in the survey.

- Even historically more volatile areas such as Consumer Electronics and Mobile Phones remain comfortably above the neutral 100-point level, indicating continued growth expectations.

These results confirm that demand is broad-based across applications, not purely driven by a single cyclical sector.

Outlook for April 2026: Slight Cooling, Still Strongly Positive

While March delivered a clear high point for sales sentiment, the forward-looking index for April 2026 suggests a moderate easing from the March peak:

- The overall index is projected to soften from 149.2 to around 144, which still represents a very strong positive environment by historical standards.

- This indicates that, although some of March’s exuberance may normalize, industry participants continue to see healthy order books and robust demand carrying into the second quarter of 2026.

ECIA emphasizes that, barring any new major disruptions, 2026 is on track to deliver one of the strongest sales climates of the past several years for the electronics supply chain.

Momentum Built on Recovery From 2025 Tariff Shock

The March 2026 results build on a multi‑month recovery trend that began in mid‑2025, after steep global tariffs temporarily pushed the index below the 100-point neutral line.

- Throughout late 2025 and early 2026, survey participants reported nine consecutive months of strong positive sentiment in both overall and category-level indices.

- By February 2026, the overall sales sentiment index had already climbed to around 140, with respondents projecting further improvement into March.

The March data confirms these expectations and highlights the resilience of the electronic components industry in the face of macroeconomic and geopolitical challenges.

Comments From ECIA Chief Analyst Dale Ford

Dale Ford, Chief Analyst at ECIA, notes that the March survey underscores the best sales environment in five years for the component supply chain

Ford highlights three key takeaways from the March results:

- Sales confidence dominates every sector of the electronic components ecosystem, from manufacturers to distributors and manufacturer representatives.

- Component categories and end markets are aligned, with all major groups posting strong positive sentiment.

- While April expectations indicate a slight pullback from the March peak, the overall index remains at a highly favorable level, consistent with a sustained period of growth.

These insights provide a reassuring signal to manufacturers, channel partners, and OEM/EMS customers planning their production and inventory strategies for the remainder of 2026.

About the ECIA Industry Pulse (ECST) Survey

The ECIA Industry Pulse survey, part of the broader Electronic Component Sales Trends (ECST) program, is a monthly and quarterly study that captures current sales sentiment and near-term expectations across the electronic components supply chain.

- The index is constructed around a 100-point baseline, where values above 100 indicate positive growth expectations and values below 100 signal contraction.

- The survey includes input from component manufacturers, authorized distributors, manufacturer representatives, and other industry stakeholders.

- Participants receive the complete ECST report, which provides detailed breakdowns by component family and end market, enabling more granular planning and benchmarking.

Organizations interested in gaining deeper visibility into market dynamics are encouraged to participate in upcoming ECST surveys or explore membership opportunities with ECIA.

Source

This article is based on information from the Electronic Components Industry Association (ECIA) March 2026 Industry Pulse / ECST communications and related published commentary by ECIA Chief Analyst Dale Ford, summarized and adapted for broader industry readership.

References

- ECIA – March Industry Pulse Survey Index Reaches Lofty Heights for Sales Sentiment

- ECIA February & Q1 2026 Industry Pulse Article (PDF)

- ECIA February 2026 Industry Pulse Signals Strong Component Growth

- ECIA: March Sales Sentiment Reaches Five-Year Record – Circuits Assembly

- Electronic Components Industry Association (ECIA) – Stats and Insights