Edgewater Research’s latest IP&E update argues that fears of a prolonged ‘hybrid for longer’ AI cycle and excessive copper exposure are overstated, while broad-based demand—especially from automotive—supports a strengthening multi‑year recovery in interconnect, passive and electromechanical components..

This May 2026 collection of news summaries, survey results, and channel market insights, covers Interconnect, Passives, and Electromechanical Components from Edgewater Research.

What’s Changed/What’s New?

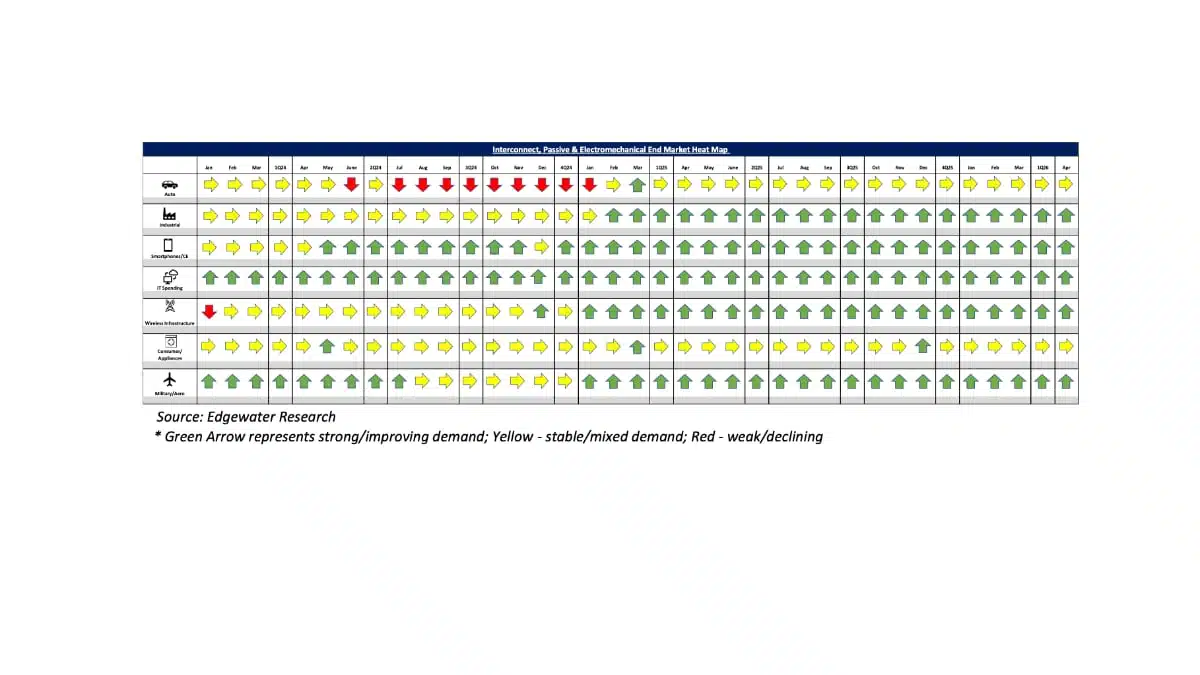

- Broader demand reads still constructive with bookings, shipments and B2B remaining elevated into Apr/May across most end mkts.

- AI customer mindset still noted as “copper when possible, optics when necessary,” with datapoints suggesting hybrid copper/optics architectures persisting through at least next two AI rack generations, implying limited risk to copper content through CY28/29.

- Full optical scale-up still seen as likely emerging first in training systems (in CY29+), while inference architectures likely remain favorable for copper longer due to localized topologies, latency sensitivity, and power-efficiency requirements.

- Passives supply continue to tighten, most notably in Capacitors, lead times extending to 52w in some cases, price increases coming.

Top 3 Channel Comments:

- There may be limited test programs before then, but we do not see optics replacing copper for intra-rack scale-up before 2029 at the earliest. The industry still faces major hurdles before CPO GPUs become practical at scale, particularly around thermal management as board-level power moves beyond 10kW.

- Optics are the future — and likely always will be — but customers will only adopt them when absolutely necessary. We have been selling embedded optics into non-datacenter applications for more than a decade, and we are comfortable with the reality that customers only move to these solutions when no practical copper alternative remains. In fact, we believe active copper adoption is likely to accelerate further before customers broadly move to optics inside the rack.

- Since the Nvidia/Corning announcement, hyperscalers have been looking for alternative fiber suppliers to secure additional supply. We hear CSPs are actively approaching alternative suppliers and believe Amphenol/CCS is likely among the beneficiaries.

Other Key Takeaways:

- Nvidia noted accepting some higher connector/backplane pricing on next-gen AI rack platforms after initially pushing for flatter pricing dynamics, implying modest content uplift opportunities for suppliers. TE is also seen benefiting from some pricing and content expansion on hyperscale AI programs.

- Kyber reads consistent M/M, with supply chain highlighting elevated risk of pushout to 2H28 due to midplane/connector challenges.

- Near term AEC datapoints constructive with Amazon issuing 2M Trn3-related RFQ, Nvidia exploring AECs for front-end networking reference design; xAI AEC demand appears paused after Feb POs, pending VR72 deployments in late 2026.

- Interest in 1.6T AEC seen as growing/broadening. META/xAI projected as major customers with neoclouds and networking OEMs noted evaluating NIC-to-ToR deployments on power, efficiency and cost advantages vs. optics.

- CSPs actively diversifying fiber supply beyond Corning, signing LTAs with alternative suppliers.

Connector/IP&E pricing in the channel cont. trending higher, with additional increases expected in Jun/Jul tied to resin, logistics, and energy inflation. YTD pricing increases noted in the double digits range, potentially driving incremental pull-forward demand. - Auto demand upticking in April across US, Japan, Korea, potentially driven by supply assurance. China Auto remains mixed.

- Tantalum capacitors effectively on allocation, MLCCs tightening, broader passive impact more mixed.

- Industrial reads broadly constructive, with semicap, automation, AI infrastructure, Mil/Aero driving strongest demand in years.

Conclusions:

The near-term IP&E outlook remains constructive, supported by elevated B2B trends, broadening demand, extending visibility, and tightening supply conditions driving both cyclical recovery and inventory replenishment. In AI/datacenter, our work continues to suggest the market is overly discounting copper durability, with supply-chain feedback still pointing hybrid copper/optics architectures persisting through the next several AI rack generations.

Taken together, we remain constructive on the broader AI datacenter interconnect and IP&E ecosystem through 2026 and likely into 2027, supported by sustained hyperscale AI investment, rising connectivity complexity, and tightening supply.