Overall ECIA’s April 2026 Industry Pulse shows sales sentiment in the electronic components market remaining robust compared to 2025, but with a clear cooling trend in expectations heading into May and the summer months.

Passive components stand out with the most optimistic near‑term outlook, while end‑market sentiment softens more sharply than component sentiment.

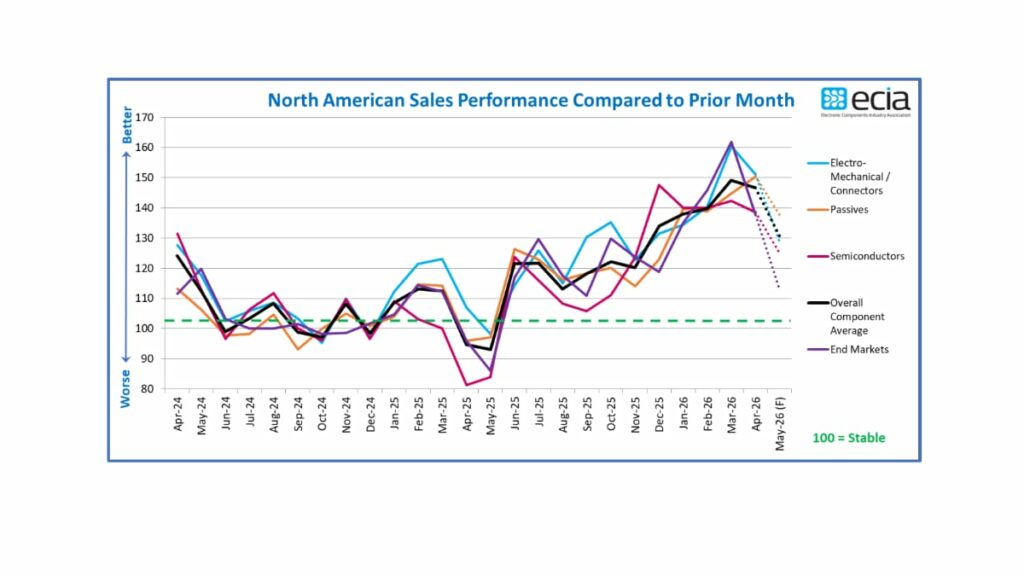

ECIA Industry Pulse April 2026 Overview

The April 2026 Industry Pulse, authored by ECIA Chief Analyst Dale Ford, reports that overall sales sentiment held strong in April at 146.6, dipping only 2.6 points from March’s sharp upswing. Despite this modest decline, current sentiment levels remain significantly higher than those seen a year earlier, underlining a still‑healthy demand environment across the authorized channel.

The survey captures perspectives from manufacturers, distributors, and manufacturer representatives across major electronic component categories and key end markets. ECIA notes that 2026 continues to track as a year of strong sales sentiment through the first five months, supporting expectations for another year of solid revenue growth if current momentum can be maintained.

Component Category Sales Sentiment

Sales sentiment by component category remained positive in April, with all major categories well above the 100 “stable” threshold. Electro‑mechanical components and connectors continued to deliver the strongest overall sentiment level at 151.1, even though this category saw a notable drop of 9.3 points compared to March.

Passive components posted a gain, with sentiment rising from 144.8 in March to 150.3 in April, highlighting strengthening confidence in this segment. Semiconductor sentiment stayed relatively steady, with only a 3.8‑point decline from March, reflecting ongoing but manageable market tightness and demand variability.

Outlook for May and Summer Cooling

Looking ahead, survey participants project a meaningful softening in sales sentiment in May, with the overall index expected to fall by 16.1 points to 130.5. Every major component category is forecast to see a sharp weakening in sentiment from April to May, with electro‑mechanical components experiencing the steepest projected decline of 22.3 points.

In this cooling phase, passive components are expected to take the lead as the most optimistic category in May with an outlook score of 137.8, still comfortably above the stability line. Even after the projected pullback, ECIA emphasizes that all component categories remain well above 100, signaling that the market is moderating from very strong levels rather than entering contraction.

End‑Market Demand and Sentiment

The most pronounced decline in the April survey appears in the end‑market assessment, where overall market sentiment fell from 161.8 in March to 137.5 in April. The outlook for May points to an additional 24.5‑point drop, bringing the end‑market index to 113.0—still positive, but significantly less exuberant than earlier in the year.

ECIA attributes much of this drop in the index to fewer respondents expecting better conditions, rather than a surge in negative assessments. Only 4 percent of survey participants viewed April as worse than March, and that share is expected to rise only modestly to 9 percent in May, with most end markets still above 100 except consumer electronics and mobile phones, which ease back toward the stability threshold.

Supply Chain Perspectives and Lead Times

All three supply chain groups—manufacturers, distributors, and manufacturer representatives—continue to report positive sales sentiment across all component sub‑categories from February through the May outlook. In a reversal from March, distributors are now the most optimistic group in their April scores, while manufacturer representatives adopt the most conservative stance, with all three groups broadly aligned with the overall average for May.

Lead time pressure intensified again in April, with 69 percent of survey participants reporting increasing lead time pressure, up from 61 percent in March. The tightest conditions remain in semiconductors, where 92 percent of respondents indicate rising lead time pressure, and reports of easing lead times are described as essentially nonexistent in the latest survey.

Longer‑Term Market Perspective

ECIA stresses the importance of context when interpreting the apparent decline from March’s peak sentiment readings. While the indices have stepped down from very elevated levels, the overall May outlook score of 130.5 is dramatically stronger than the 93.1 reading recorded in May 2025, when sentiment fell below 100 for two consecutive months.

The association remains optimistic about the longer‑term outlook, pointing to continued innovation and adoption of next‑generation technologies as drivers of both corporate and consumer demand. ECIA expects that these structural growth factors will support healthy electronics component demand beyond the current survey horizon, provided the industry continues to manage capacity, lead times, and supply‑demand balance effectively.

Source

This article is based on information and data provided in the ECIA Industry Pulse April 2026 Outlook article prepared by ECIA and Chief Analyst Dale Ford, summarizing survey findings across the electronic components supply chain.

References