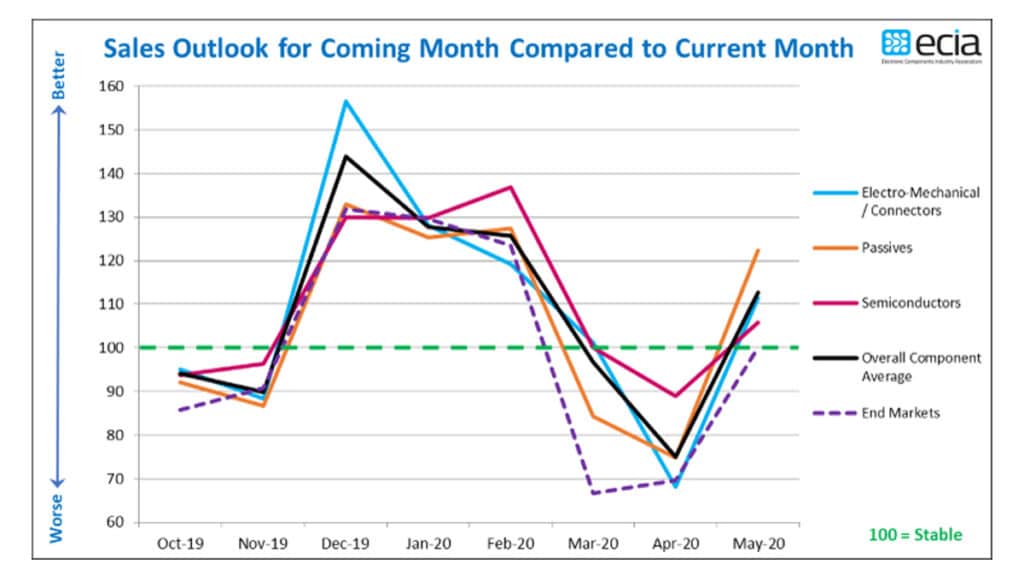

There may be a reason for industry optimism in June sales compared to May 2020. According to a recent survey of Electronic Components Industry Association (ECIA) members, the electronic component sales expectation jumped to nearly 113 for the month of June compared to May.

Improved sales expectations were reported for every major component category including electro-mechanical/connectors, passives and semiconductors. Further, the overall average outlook for sales by major end markets recovered back to a “stable” level of 100 in the index.

The strongest end market sales expectations are found in the medical equipment, telecom networks and avionics-military-space sectors. However, even markets facing a more challenging environment are expected to improve in June, the report noted.

The electronic components industry had an exceedingly difficult market in 2019. But expectations were high for the start of 2020 and then the COVID-19 pandemic hit hard. The gradual reopening of the economy has prompted greater optimism for June.

The expectations for the latter half of the year of 2020 are looking better. For example, the World Semiconductor Trade Statistics (WSTS) has released its new semiconductor market forecast generated in May 2020. The WSTS expects the world semiconductor market to be up by 3.3 percent to US$ 426 billion in 2020. This reflects expected increases in Integrated Circuits (ICs), except analog, with an increase from memory at 15.0 percent, followed by logic with 2.9 percent. In 2020, Americas and Asia Pacific are expected to grow.

Further out in 2021, the growth of global semiconductor fab equipment sales is looking up. According to an update of the SEMI World Fab Forecast report, spending on equipment will see a 24 percent growth to a record US$67.7 billion. Memory fabs will lead worldwide semiconductor segments with US$30 billion in equipment spending, while leading-edge logic and foundry is expected to rank second with US$29 billion in investments.

The report also predicts rising investments in the second half of 2020, although the year will still mark a drop in fab equipment spending by 4 percent. This follows a steep drop of 8 percent in 2019.

It’s hard to predict how change in equipment spending will affect specific products. The reports suggest that ongoing pandemic-related layoffs and rising unemployment will lead to falling smartphone and new car sales while the need to communicate will still drive industry growth as cloud services, server storage, gaming and health applications spur demand for memory and IT-related devices.