November 2023 collection of news summaries, survey results and channel market insights on Interconnect, Passives & Electromechanical Components from Edgewater Research.

Limited Change Month/Month with Relative Stability in Demand and Pricing

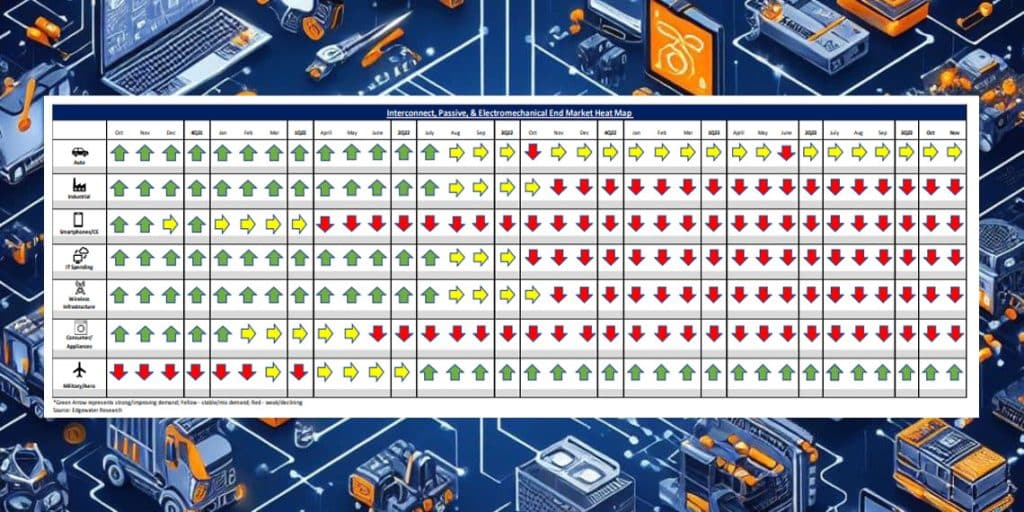

Key Takeaways:

1. 4Q through mid-Nov seen as in-line with continued weakness in distribution and mixed but more stable demand direct.

2. Bookings feedback mixed by end market with stability in Auto, strength in Mil/Aero/AI, and cont. weakness in the rest.

3. 2024 outlooks still muted at LSD growth and tied to 2H recovery expectations with disti demand projected underperforming direct.

4. China still viewed as weak but now more stable compared to weakening trends in the West.

5. Europe 4Q trending weaker on earlier than expected factory shutdowns in Dec, reducing shipping days in the quarter.

Top 4 Channel Comments:

• We (a connector supplier) are projecting a flattish 2024 after a high-single-digit decline in 2023. Auto is the only bright spot for us, and we project that offsetting the muted outlook in other markets. Our participation in AD&M is limited and not a material tailwind.

• In EMEA, most Industrial/Auto customers are shutting down factories for retooling on 12/18. Effectively we will have 1 less week on top of Christmas week of no shipments. We are staring at a 10% headwind from fewer shipping days vs. last year.

• So far, we have seen only the first wave of EV pushouts in N.A. We believe there will be further rationalization. The cars don’t sell well, and the new UAW deal makes a lot of them more unprofitable. Some are now not even projected to break even for years. It is hard to put good money into bad projects. We are bracing for a tough 2024 in N.A. Auto

• Auto demand globally remains a lone bright spot in the connector industry. We (a supplier) believe we can get another year of double-digit growth in a flat production year based on the content growth from the programs we have.

Other Key Takeaways:

6. Competitive pressure in Europe distribution seen ramping up by Chinese suppliers; forcing suppliers to cede share and/or cut margins.

7. Auto connector demand and outlook more stable vs. semis on healthier inventory and fewer double bookings in backlogs. Forecasts for 2024 range from mid-single digit to low double-digit growth on content gains, stable pricing and flattish global production.

8. US Auto feedback mixed. Near-term demand seen stable with no UAW impact thus far and manageable headwinds from EV delays due to lower mix. Anecdotally the supply chain notes compatibility issues for Yazaki connectors at Stellantis EVs.

9. MT N.A. Auto outlook more cautious as current EV delays seen as only the first wave due to profitability concerns tied to UAW.

10. China Auto demand more constructive on new models, production ramp up, and strong xEV 2024 outlook and, in contrast to semis, limited inventory overhang.

11. In Auto some productivity gains pass-through not ruled out but overall, 2024 pricing seen as stable, in part due to lack of an aggressor.

12. Industrial/Comm Transport/IT/Telco feedback little changed – mostly weak and projected to persist into 1H24. Mil/Aero still strong.

Conclusion

Following the M/M step down in industry fundamentals we experienced in October, November fundamentals appear largely stable. Demand is relatively unchanged M/M and still viewed as weak/sub seasonal as the inventory continues to work through stubbornly high inventory levels.

Pricing is mixed, with relatively stable pricing noted within interconnect, especially vs. the continuing pricing pressures in passive and emerging pricing concessions within semis. We continue to remain cautious on IP&E fundamentals overall, but would not we are more cautious on passive fundamentals vs. interconnect fundamentals, which we do believe will experience a rebound earlier than semis and passives as the interconnect suppliers 1) did not experience as significant shortages and inventory build and 2) the interconnect suppliers were not nearly as aggressive with NCNR programs.

Full report available from:

Dennis Reed, Sr. Research Analyst, Edgewater Research