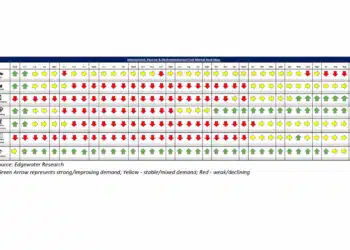

March 2024 component distribution insights by Edgewater Research shows modest directional improvements in sales, distributors broadly seen implementing costs savings initiatives.

Key Takeaways:

- Semi POS viewed as remaining soft, showing limited signs of improvement post CNY with B2B remaining at 0.8-0.9x. IP&E demand better with clear signs of pick up in turn orders and B2B broadly around parity.

- Inventory seen directionally improving in 1Q on most suppliers relaxing NCNRs. Semi inventory still viewed as challenging, with digestion potentially stretching into 2H. STM inventory consistently noted as worst in shape, well above targets and averages.

- Analog Devices seen restructuring staff tied to Arrow and targeting $800M to $1B in sales shift direct over the next 12 months.

- Arrow seen laying off ~2K employees in 1Q across layers and geos, with focus on staff supporting TXN/ADI product lines.

- Avnet is seen laying off ~250 Farnell employees globally in 1Q and shifting a substantial portion of US customer support to the UK.

- Arrow’s 4Q inventory drawdown seen driven by aggressive NCNRs, leading alienated customers to pivot future demand away.

- Avnet is seen as continuing to outperform Arrow gaining share sequential in Americas and EMEA. In IP&E, Avnet also seen outperforming over the last 6 months, gaining share with key lines from TE, Amphenol, Yageo, AVX, others.

- TTI seen as outperforming broadline competitors, product mix (IP&E vs. semi), end market exposure and consistency in market viewed as driving outperformance.

- High service distribution remains challenging, albeit customer counts viewed as showing improvements.

Top 3 Channel Comments:

- Demand in China is challenging, we are starting to have doubts if we will see a recovery this year. The year looks very similar to last when we were expecting a 2H recovery at this time but it never came, except in pockets like Auto.

- We saw clear signs of Arrow pushing product at the end of 4Q, mostly via NCNRs to customers. By doing that Arrow pissed off a lot of customers. The trend is not new but the actions in 4Q reached a tipping point. This opens the door for Avnet. Arrow could have permanently shut the door for Avnet after the SAP debacle in 2016-2017 but now they are giving customers a reason to return to Avnet.

- A year ago, Arrow was outperforming Avnet in IP&E, today the dynamic has flipped. Avnet has executed better, gaining share with key lines like TE, Amphenol and some of the large passive suppliers like Yageo, and AVX.

Conclusion:

Distribution fundamentals remain challenging as the industry continues to grapple with elevated inventory levels, most notably in semiconductors.

While semis remain problematic, we continue to see signs of progress on IP&E inventory which we believe is leading to outperformance of distributors more leveraged IP&E vs. semis. With inventories elevated and sales muted, we are seeing an increased focus on cost reductions across distributors.

Full report available from: Dennis Reed, Sr. Research Analyst, Edgewater Research

Source:

Edgewater Research