Source: Murata news

Murata releases its FY2019 2nd quarter consolidated results from period July 1, 2019 to September 30, 2019.

In Summary

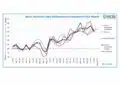

- Net sales in Q2 increased 12.8% from the previous quarter thanks to strong sales of modules, capacitors, and other components for new smartphone models despite a decrease in the sales of capacitors for distributors due to the impact of inventory adjustment.

- Net sales for H1 decreased 3.5% year on year due to a fall in the sales of capacitors, surface acoustic wave (SAW) filters, and lithium ion batteries for smartphones and the impact of the strong yen despite the growth in the sales of capacitors for automotive use and base stations.

- Operating income in H1 reached the target for the period thanks to efforts for cost reduction and improvement in the product mix despite posting an impairment loss of 19.8 billion yen due to a decline in the profitability of batteries for mobile devices. Operating income decreased 12.9% year on year and operating income ratio fell by 1.7 percentage points year on year to 16.0%

- Net sales are expected to be 1,510.0 billion yen (down 4.4% from the previous forecast) and operating income is projected to be 230.0 billion yen (up 4.5% from the previous forecast).

Projections and Application Trends can be followed in more details at Murata’s presentation available to download from their website here.