Edgewater researchers report IP&E demand and pricing are strengthening on the back of AI and industrial recovery, with tight passive component supply and a likely shift to hybrid copper‑plus‑optical datacenter architectures that keep intra‑rack copper dominant through 2030.

This February 2026 collection of news summaries, survey results, and channel market insights, covers Interconnect, Passives, and Electromechanical Components from Edgewater Research.

What’s Changed/What’s New?

- Broader 1Q demand tracking better. Bookings momentum accelerating in Jan/Feb, B2B ~1.15-1.2x, driving backlog rebuild.

- TE/Amphenol leading second round of channel price increase YTD (+7-8% effective 3/2), impacting new orders and backlog, other

suppliers expected to follow. - AWS Trainium CY26 forecast raised 30–40% to 2.3-2.4M ASICs; now estimating ~2x connector TAM growth Y/Y vs ~+50% prior.

- First-wave CPO more likely to expand scale-up across racks/pods rather than displace intra-rack copper. CPO-based GPUs and

optical backplanes likely to move into focus, but deployment timing and scope are noted as key variables. - Hybrid copper/optics scale-up approach appears more likely over the next 3–5 years, with copper retaining intra-rack dominance.

- Kyber midplane + CPC on NVSwitches viewed as marginally more likely for Rubin Ultra; Oberon-style 72×2 with cabled backplane

and CPO for rack-to-rack connection noted as a backup. Scenarios suggest copper content flat at worst, meaningfully higher at

best.

Top 4 Channel Comments:

- We believe Nvidia’s messaging will shift from “copper-only” toward a hybrid copper/optics scale-up model. CPO is likely to be

featured prominently at GTC, but we do not see copper being displaced inside the rack anytime soon. The more probable path is

optics for rack-to-rack links, while copper remains dominant intra-rack due to cost and practicality. - Despite growing CPO push from large silicon suppliers, CSPs remain conservative. We expect adoption to ramp gradually from low

single-digit penetration (5–10%) and do not see in-rack optics reaching 30–40% until 2030 or later. For example, we have a hard time

envisioning Amazon to adopt CPO/optics inside the rack aggressively given its historically cautious stance on architectural shifts. - Nvidia may push CPO aggressively over the next year or two, but we question how much will materialize. We don’t see an immediate

need over the next 3–4 years as 1) copper can still meet density and speed requirements, and 2) even a 2% yield loss from integrating

CPO onto a ~$60K AI ASIC implies ~$1,200 of scrap per chip. For those reasons, we don’t see CPO on AI ASICs until 2030. - Recent Coherent and Lumentum commentary on 2H27 CPO platforms likely tied to AMD’s next-gen rack. At Nvidia, meaningful scaleup adoption appears aligned with Feynman. Even for AMD, the initial CPO config is likely test platforms, not mass deployment.

Other Key Takeaways:

- CPC emerging as copper multiplier; full-stack architectures (switch + AI ASIC + backplane) imply ~2–3x content.

- Trn4 has a full-stack CPC + backplane configuration, likely based on TE, though final volume architecture remains undecided.

- Nvidia CY26 rack forecast unchanged at 60–80K. TE backplane ramp for GB300 seen as progressing through March.

10.VR72 compute tray midplane connectors now 100% Amphenol; VR72 content estimates little changed.

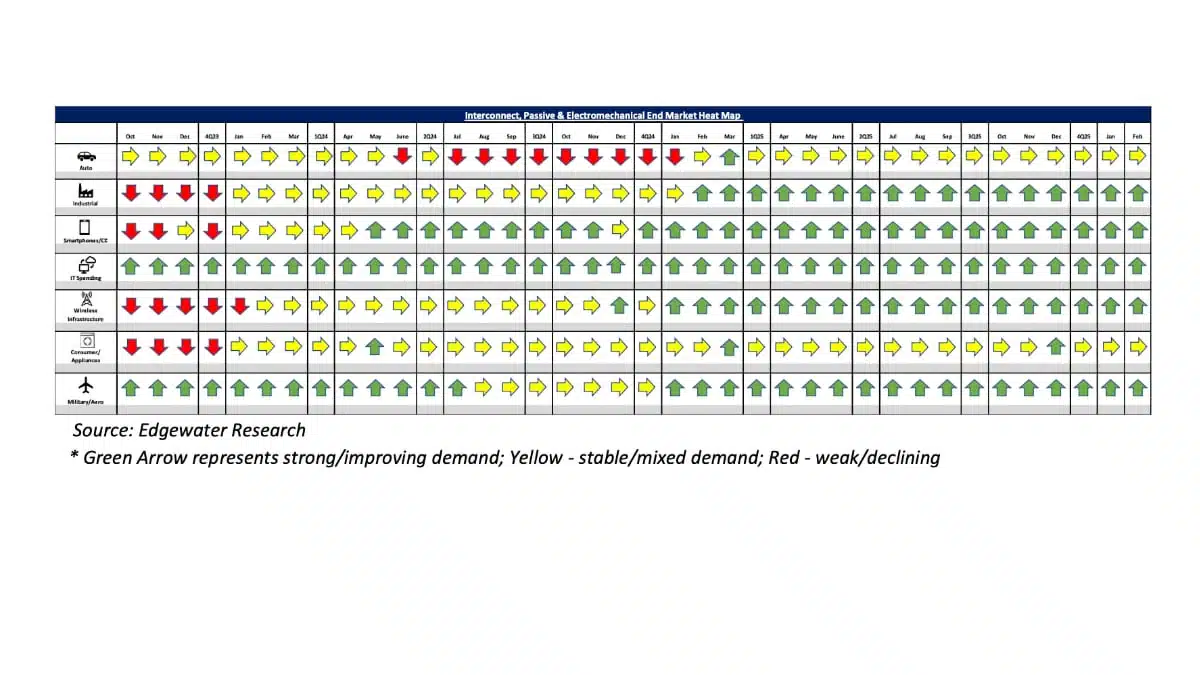

11.Passive lead times extending, pricing firming; Tantalum capacitors tightest, resistor pricing firming on silver exposure.

12.Industrial recovery broadening beyond energy; bookings strength increasingly diversified across automation, semicap and HVAC.

13.Auto CY26 base case unchanged at mid-single-digit growth, with pricing doing more heavy lifting than production.

Conclusion:

- IP&E fundamentals continue to improve through 1Q with demand and pricing firming, supporting stronger bookings and improving

B2B ratios. Encouragingly, strength is broadening beyond AD&M and IT Datacom, while OEM/EMS customers appear to be shifting

from inventory drawdown toward supply sufficiency. At the same time, hyperscale AI spending remains a major driver, with datacenter

demand continuing to strengthen. Overall, we are increasingly constructive, projecting double-digit growth for the IP&E industry in

2026 absent macro disruption. On the copper vs optics debate, supply-chain feedback suggests the near-term risk to intra-rack copper

is overstated. While CPO development will continue, deployment is likely to be phased. The most likely outcome over the next several

years is a hybrid copper-plus-optics architecture, with optics used for rack-to-rack links while copper remains dominant inside the

rack, particularly as CPC architecture helps extend copper’s performance and content in next-generation systems.

Full report available from: Dennis Reed, Sr. Research Analyst, Edgewater Research

Source:

Edgewater Research