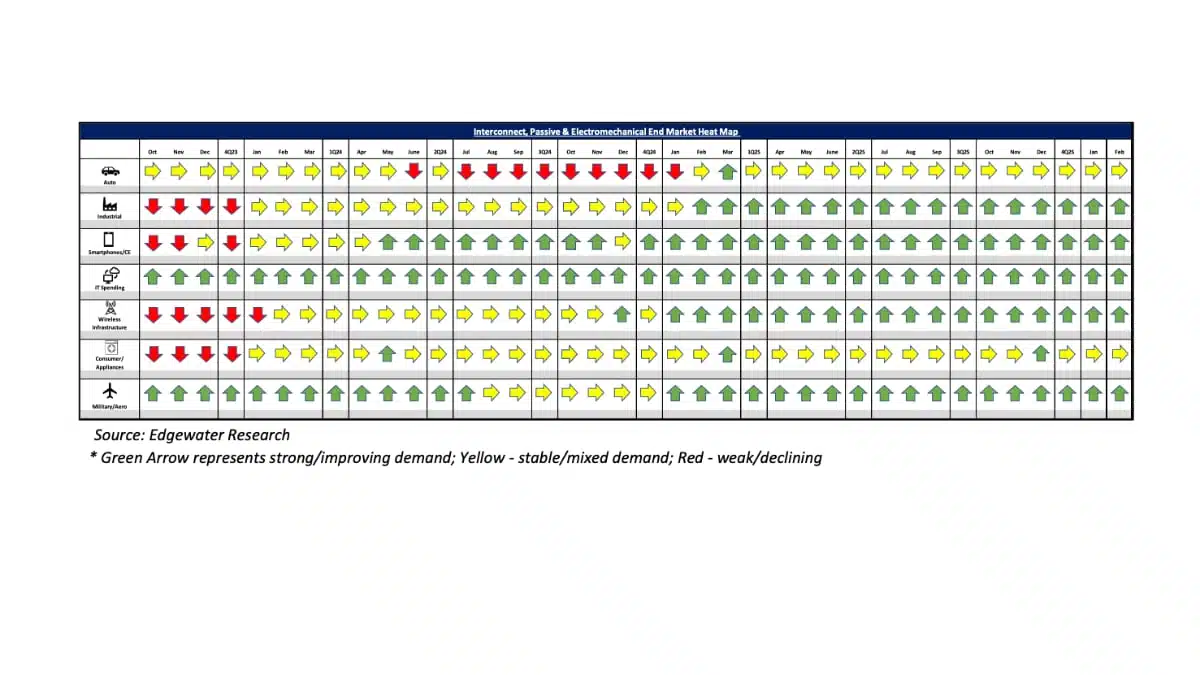

Edgewater Research’s IP&E report indicates that the recovery trend continued to strengthen through the end of 1Q, with book-to-bill ratios moving higher. Meanwhile, the debate over optical versus copper interconnects remains active in AI applications.

This March 2026 collection of news summaries, survey results, and channel market insights, covers Interconnect, Passives, and Electromechanical Components from Edgewater Research.

What’s Changed / What’s New?

- Broader demand continues to improve, with recovery momentum widening across end markets and supporting IP&E fundamentals and pricing efforts amid rising material and logistics costs.

- Bookings are still accelerating month over month. B2B is now seen in the 1.25–1.35x range versus 1.15–1.20x last month, and the supply chain is increasingly convinced the industry is in the early innings of a broad-based recovery.

- The Kyber design remains fluid and is expected to evolve following GTC, with potential CPC and other copper/connector content additions.

- The Kyber midplane connector is likely shifting to an Nvidia-driven design, which should enable multi-sourcing, with an estimated 3–4 suppliers sharing allocations.

- Nvidia’s new platforms (Groq LPX, Vera 256, storage) are expected to leverage Amphenol’s HD Paladin backplane, creating incremental copper TAM estimated at roughly 650 MUSD in CY27, assuming a 25% attach rate to compute racks and 10–20 kUSD per rack in backplane content.

Top 4 Channel Comments

- Hyperscalers are likely to begin deploying optical backplanes over the next 1–2 years to generate reliability data; however, large-scale deployment of optics inside the rack is not expected until the technology is proven in volume use. Copper remains sufficient for many AI scale-up applications.

- Current XPO implementations are paired with flyover/CPC links from the switch ASIC to the front panel because this is a new standard and traditional PCB traces are not viable. To support 224G and the next generation at 448G, PCB traces are effectively off the roadmap.

- Early in 2026, demand and bookings are ahead of expectations, pricing is firmer, and supply has tightened. B2B in January was 1.3x vs. 1.1x in December, and February increased further to 1.35x. Monthly shipments in February were the strongest in three years, which is notable given the fewer shipping days.

- So far, the industry has seen two direct effects from the war in the Middle East. Some lead times have increased because certain shippers are now bypassing the Suez Canal out of caution, adding roughly four weeks to transit times. Insurance premiums and freight rates have also risen sharply. While a direct impact on demand has not yet been observed, the industry is watching how higher oil prices may influence resin pricing and the availability of key chemicals used in resin production.

Other Key Takeaways

- FIT is viewed as securing a license to manufacture Amphenol connectors for Nvidia’s backplane/VR72 midplane, though FIT’s ramp timing and specific use cases remain unclear.

- Amazon is also seen leaning toward a similar hybrid copper/optical scale‑up architecture for Trn4, potentially with a multi‑SKU approach.

- The industry transition to optics within the rack is still expected to be phased. In AI, copper is likely to shift from a pure content story to more of a unit‑growth‑driven story.

- Broad CPO adoption in Nvidia scale‑up platforms is viewed as limited until around 2028; Kyber 1152 design details remain TBD, with a likely copper‑plus‑optics intra‑rack approach.

- Near‑term CCS datacenter revenue is expected to be driven by scale‑out, cluster size, and topology. Current estimates suggest several hundred dollars of passive fiber content per GPU, with CPO, multi‑plane architectures, and larger clusters potentially lifting content to above 1,000 USD per GPU over time.

- Trn 3 demand remains around 2.3–2.4 million units, or roughly 60,000 racks in CY26. Connector TAM is little changed month over month and is projected to grow 100–120% year over year in CY26.

- TPU CY26 forecasts remain unchanged at 68–69 thousand racks, with CY27 projected at approximately 100 thousand racks or 6–7 million TPUs.

- META and xAI continue to lead scale‑out Ethernet AEC usage in Nvidia deployments, with xAI’s AEC attach rate estimated at more than 3:1 per GPU.

- Industrial markets are inflecting positively, with broad-based strength and rising bookings supporting upside to CY26 growth expectations.

- Automotive in CY26 remains stable but not improving; the outlook is still for mid‑single‑digit growth, with persistent downside risk.

- Near‑term impact from Middle East disruptions is seen as limited, but medium‑ to long‑term effects from longer shipping routes and higher raw material costs could put further pressure on lead times and potentially drive additional price increases in 2026.

Conclusion

IP&E fundamentals are improving month over month, with mounting bookings momentum pushing B2B ratios higher and the recovery broadening across multiple industrial subsegments. Strength in Datacenter/AI remains robust, while Automotive continues to lag. The ongoing improvement in fundamentals is supporting pricing across suppliers and product categories, further underpinning a constructive outlook for 2026. Assuming no major macro or geopolitical shocks and no significant demand disruptions (for example from memory shortages), the industry appears well positioned to deliver double‑digit growth.

Full report available from: Dennis Reed, Sr. Research Analyst, Edgewater Research