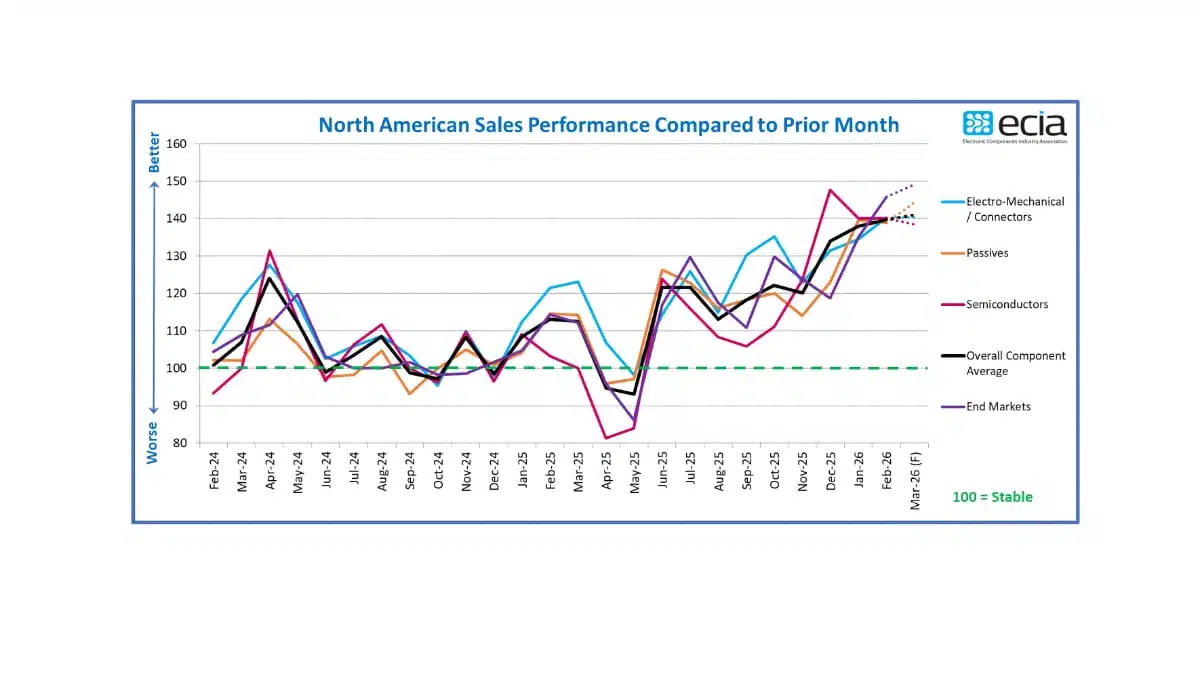

ECIA’s latest Industry Pulse survey for February 2026 confirms that sales optimism continues to climb across every major sector of the electronic components market.

Average sales sentiment reached 139.7 in February, up from 138.0 in January, marking the ninth consecutive month of strong positive sentiment and the fifth month in a row with robust results across all subcategories.

Strong Sales Sentiment Across Components and Channels

The survey highlights a solidly positive environment in all major component categories, including semiconductors, electro-mechanical/connectors, and passive components. A score of 100 represents the break-even line between negative and positive sentiment, and all categories remain well above this threshold.

Looking ahead, respondents project further improvement, with the March 2026 overall sentiment index expected to reach 141.1. After a steep drop in confidence triggered by global tariff shocks in 2025, the market has recovered strongly since June, and industry participants now expect 2026 to maintain a healthy sales climate, barring any major unforeseen “Black Swan” disruptions.

Q1 and Q2 2026 Outlook: Broad Growth, Minimal Negativity

Quarterly survey results for Q1 and Q2 2026 support a sustained growth narrative through at least the first half of the year. In Q1, 71% of respondents report positive sales growth, rising slightly to 72% for Q2.

Negative expectations are now the exception rather than the rule, with only 2% of participants in Q1 and 4% in Q2 anticipating declining sales. Remarkably, no respondents in the semiconductor segment report expectations of negative growth in either Q1 or Q2, underscoring the sector’s current strength.

Distributors Lead in Optimism, But All Channels Positive

Sentiment varies by channel, but all remain clearly positive. Distributors report the strongest confidence levels for both February and March, with an overall average around 160 on the sentiment index.

Manufacturers and manufacturer representatives are more conservative, but still firmly optimistic, posting index scores between 119 and 130 for the same period. Despite the gap between channels, all three groups—distributors, manufacturers, and reps—report positive sentiment in every product subcategory in both February and March.

End-Market Trends: Industrial and Aerospace Lead, Consumer Also Strong

The overall end-market index rose to nearly 146 in February, its highest reading since May 2021, and is expected to climb further to 149.2 in March. This broad-based strength spans all end markets covered in the survey.

Avionics, military, space, and industrial segments continue to post the highest sentiment scores, reflecting sustained investment in mission-critical and infrastructure-related applications. Even at the lower end of the spectrum, markets such as consumer electronics and mobile phones still deliver index readings above 122, indicating healthy demand and far from any contraction signal.

Lead Times: Easing in Semiconductors, Persistent Concerns in Advanced Memory

Lead time dynamics remain a critical operational indicator for the industry. In February, pressure eased notably in semiconductors, as the share of respondents reporting increasing lead times dropped from 52% to 39%.

For electro-mechanical and passive components, lead times were generally stable between January and March, with very few reports of improvement. Only 2% of respondents cited decreasing lead times for electro-mechanical components, and 5% for semiconductors. A significant supply–demand imbalance in advanced memory ICs continues to be one of the most pressing risks, as constrained availability in this segment could stall sales in other parts of the components market and has become a key focus area for supply chain management heading into 2026.

Source

This article is based on information from the Electronic Components Industry Association (ECIA) Industry Pulse and Electronic Component Sales Trends (ECST) survey summary for February and Q1 2026, authored by ECIA Chief Analyst Dale Ford.