TTI MarketEYE has published a new analysis by Dennis M. Zogbi, Paumanok Inc., that examines how recent movements in ruthenium prices are reshaping the global passive components supply chain, with a specific focus on thick film chip resistor technology and related raw material ecosystems.

The article highlights how this key platinum group metal has become a strategic factor for manufacturers, distributors and end customers in high‑volume electronics production.

Ruthenium as a Strategic Raw Material

Ruthenium is widely used as a critical resistive element in thick film chip resistors, where it is typically employed in the form of ruthenium oxide within screen‑printed resistive pastes on ceramic alumina substrates. These thick film resistor products are manufactured in extremely high volumes and are consumed across virtually all printed circuit boards, making ruthenium demand closely tied to overall electronics production. This linkage has elevated ruthenium from a niche material to a strategic commodity within the passive components industry.

Price Volatility and Supply Dynamics

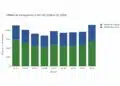

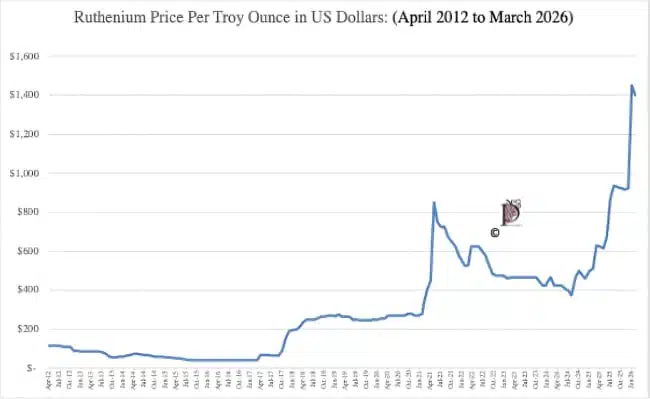

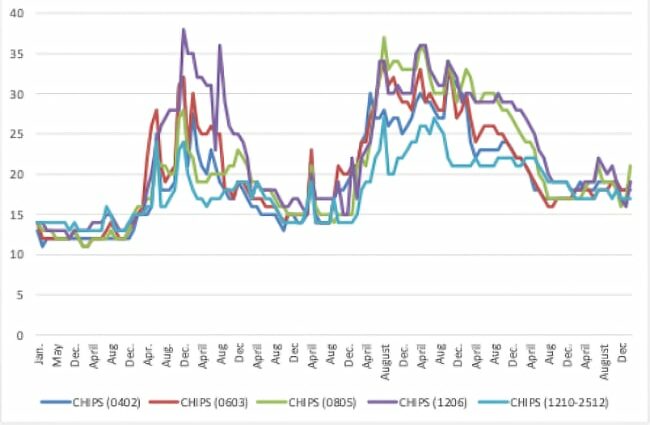

In recent years, ruthenium has experienced pronounced price volatility, driven by changing conditions in the platinum group metals supply chain, mine operations and global demand from both electronics and other industrial sectors. Historical data show that price spikes can be rapid and substantial, with previous cycles seeing ruthenium rising from double‑digit to several hundred US dollars per troy ounce within a relatively short period. This volatility directly influences the variable cost structure of thick film chip resistors, where raw materials account for a significant share of total manufacturing cost and therefore have an immediate impact on margins and pricing strategies.

Impact on Thick Film Chip Resistors

Because thick film chip resistors rely so heavily on ruthenium‑based resistive pastes, fluctuations in metal prices can quickly translate into changes in lead times, price offers and overall availability. During past periods of tightness, elevated ruthenium prices have been associated with longer lead times and selective price increases on mass‑produced resistor ranges that are most exposed to ruthenium consumption. This sensitivity is amplified by the massive global production volumes of thick film chips, which number in the trillions of pieces annually and therefore consume a substantial share of the ruthenium available to the electronics sector.

Alternative Resistor Technologies and Design Options

One of the key themes is the way price volatility in ruthenium encourages customers to consider alternative resistor designs where technically and commercially appropriate. Thin film chip resistors based on nickel or other base metals can be considered as an important option, offering lower exposure to precious metal markets and often improved electrical performance, albeit at different cost structures and with more limited economies of scale. In previous shortage cycles, thin film chips have been successfully used as one‑to‑one replacements in certain case sizes and resistance ranges, giving procurement teams an additional lever to manage risk alongside traditional thick film sourcing.

Ruthenium Dependency: The Risk Factor You Can’t Ignore

Thick film chip resistors are the real workhorses of modern electronics. Low-cost and nearly omnipresent, they are used in the trillions every year because every circuit needs accurate resistance values to operate, and these components provide them in a highly compact format built from ceramic, glass, ruthenium and silver. In terms of sheer manufacturing and usage volume, only multilayer ceramic chip capacitors come close.

They appear in almost every electronic circuit worldwide. Key end uses include mobile phones, PC motherboards, hard disk drives, displays, automotive electronic modules, televisions, audio amplifiers and industrial control systems – in short, virtually any product containing a printed circuit board.

These enormous production scales, combined with very low selling prices and a highly concentrated supplier base, make thick film chip resistors some of the most difficult components to manufacture and source consistently. Their strong structural reliance on the platinum group metals supply chain – via their long-established dependence on ruthenium – creates substantial, hard‑to‑control cost pressure. With ruthenium prices remaining unstable, this dependency is becoming one of the most significant emerging risk factors for the wider high‑technology sector in the coming financial year.

Variable Raw Material Costs

The fluctuating cost of raw materials makes passive components relatively distinctive, because their supply chain must, to a large extent, depend on external merchant suppliers and specialized materials processors to deliver the formulated powders and pastes used to manufacture these devices.

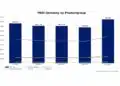

Over time, shifts in metal pricing and availability have been the dominant risk drivers in the manufacturing cost of high‑volume capacitors and resistors, both produced in the trillions of units. In recent months, ruthenium prices have climbed to heights not seen in many years.

On average, variable raw material inputs represent about 44% of total production costs for the global resistor industry. Any significant increase in the prices of feedstock metals used here will ultimately feed through to thick film chip resistor prices and product availability.

Summary and Conclusion

This volatility has pushed customers toward alternative resistor technologies based on thin‑film nickel. However, thin‑film resistors are produced on a far smaller scale than thick‑film chips, one of the highest‑volume electronic components globally (measured in the trillions of units). Resistors consume a notable portion of global ruthenium output (which also serves in cracking catalysts, HDD coatings and specialized chemicals). As a result, the metal is highly responsive to shifts in resistor demand, and its behavior as an indicator of conditions in the global high‑tech economy should be carefully monitored by analysts of precious‑metal markets.

Outlook

For thick‑film resistor makers using ruthenium‑bearing inks and for chip resistor suppliers, ruthenium now poses the most severe cost headwind in decades. The future supply picture depends strongly on Russian output, which remains restricted by sanctions, and on South African production, which continues to suffer from power shortages (Eskom load‑shedding) and labor disruptions.

With no true technical substitutes that match ruthenium’s performance in precision resistor applications, producers are forced into three main options:

- (1) absorb structurally higher costs,

- (2) redesign pastes to reduce ruthenium content,

- (3) pass price increases downstream.

In this context, ruthenium requires close supply‑chain monitoring and proactive inventory and sourcing strategies.

Source

This article is based on information and analysis presented in a TTI MarketEYE article authored by Dennis M. Zogbi, together with related background materials on ruthenium usage in passive electronic components and historical raw material trends.

References

- TTI MarketEYE – Ruthenium’s Critical Role in the Passive Components Supply Chain

- TTI MarketEYE Resource Center – Passives

- TTI MarketEYE – Passive Component Raw Material Index

- Paumanok/Passive-Components.eu – Resistor Markets Tighten as Ruthenium Prices Skyrocket

- Passive-Components.eu – Thick Film Chip Resistors: Spotlight on a Rendered Economy

- Passive-Components.eu – Ruthenium and Other Metals for High-Volume Passive Electronic Components