Edgewater researchers report that January 26 component distribution recovery takes hold as orders inflect; outlook is improving.

What’s Changed/What’s New?

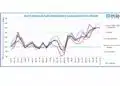

- Shipments and orders have been increasing since October, particularly in the West, which is driving a positive outlook for the fourth quarter. B2B orders have grown by approximately 1.1 times, visibility has improved, and lead times have increased.

- The distribution outlook for 2026 has been revised upwards to a high-single-digit growth rate, driven by AI/DC, military/aerospace, and improving industrial demand.

- The first-quarter outlook is seasonal to above-seasonal in the West (Americas and Europe), with quarterly growth projected to be between 3% and 5% and a year-over-year growth rate of approximately 10%. This supports the momentum of the early cycle.

- The distribution inventory mix is still challenging. The company is relying on in-demand SKUs as lead times extend, while slower-moving semi-conductors remain elevated.

- Arrow’s performance in Asia-Pacific is expected to improve from the consolidation of Analog Devices starting in the first quarter. This is expected to generate approximately $500 million in annualized revenue by 2026, although this is partially offset by the continued shift of direct-to-consumer sales from TI.

- The shift of AI-related builds from the United States to Mexico is expected to benefit Arrow, potentially supporting the recent performance of Arrow in the Americas.

- TE is shifting some automotive sales to distribution, which is estimated to create approximately $200 million to $300 million in incremental channel opportunities. Arrow and Avnet are positioned to benefit from this shift. Supply Chain Services programs are regaining traction due to the disruption caused by Nexperia, which could serve as a catalyst.

- The high-service distribution segment continues to outperform the broadline segment, often driven by inventory availability. Private distributors are outpacing the growth of public distributors. Farnell’s synergies with Avnet’s core business are gaining traction, and their performance is improving.

Top 3 Channel Comments:

We haven’t felt as optimistic about the market outlook in a while. B2B has improved to 1.1 times, the backlog is healthy, and we are projecting roughly 10% growth in 2026.

In recent quarterly reports, Arrow and Avnet expressed more positive sentiments, stating that the recovery is on firmer footing. Both companies cited better-than-expected fourth-quarter bookings, improving backlogs, and B2B orders around 1.1 times, with quarterly growth projected in the West and high-service distribution growth for the entire year.

Distribution inventory is improving, but not as quickly as expected due to mix issues. The inventory available does not match customer demand. Although the drop in orders is still elevated, it is becoming increasingly difficult to fulfill them within the quarter as supplier lead times have increased to approximately 12 weeks.

Distribution Background Information:

| Sales by HQ Geography | |||||

|---|---|---|---|---|---|

| 2021 | 2022 | 2023 | Y/Y | ||

| Americas | $67.0 | $74.9 | $71.9 | -4% | |

| Taiwan | $60.9 | $55.9 | $54.1 | -3% | |

| China | $30.8 | $28.8 | $23.8 | -17% | |

| Japan | $20.9 | $21.6 | $21.7 | 0% | |

| Europe | $4.5 | $4.9 | $5.0 | 3% | |

| Singapore | $1.1 | $1.1 | $0.5 | -56% | |

| South Korea | $0.6 | $0.8 | $1.0 | 31% | |

| Total | $188.1 | $196.4 | $178.0 | -9% | |

| Sales by Components | 2020 | 2021 | 2022 | 2023 | Y/Y |

|---|---|---|---|---|---|

| Semis | $114.1 | $148.0 | $147.8 | $139.9 | -5% |

| Interconnect | $11.8 | $14.3 | $13.7 | $11.7 | -14% |

| Passives | $8.2 | $10.0 | $9.6 | $9.6 | 0% |

| Electro-Mech | $5.7 | $7.0 | $7.0 | $7.5 | 7% |

| Computer/System | $1.6 | $1.9 | $5.8 | $2.8 | -51% |

| Power & Batteries | $1.3 | $1.7 | $2.1 | $1.6 | -23% |

| Other | $4.3 | $5.5 | $2.1 | $5.0 | 141% |

| Total | $147.1 | $188.1 | $196.4 | $178.0 | -9% |

Conclusion

Macro data points generally align with our IP&E and semi-work, with some nuanced channel implications. Distributors seem well-positioned to capitalize on the cyclical upturn, pockets of TAM-to-DTAM conversion, and renewed momentum in supply-chain services.

Rising lead times and recurring supply chain disruptions are driving greater demand for planning and fulfillment support. However, near-term inventory mix challenges and heightened competition are expected to persist, potentially dampening margin recovery beyond opportunistic upside tied to memory shortages.

Overall, we remain constructive on the sales recovery, but we have a more measured view of the pace and magnitude of profit improvement for component distributors.

Full report available from: Dennis Reed, Sr. Research Analyst, Edgewater Research