ECIA’s January 2026 survey signals the strongest sales sentiment for the electronic components industry in more than four and a half years. The January 2026 results show broad-based confidence across product categories, end-markets, and all major supply chain channels as the industry enters the 2026.

Overall Sales Sentiment at Multi‑Year High

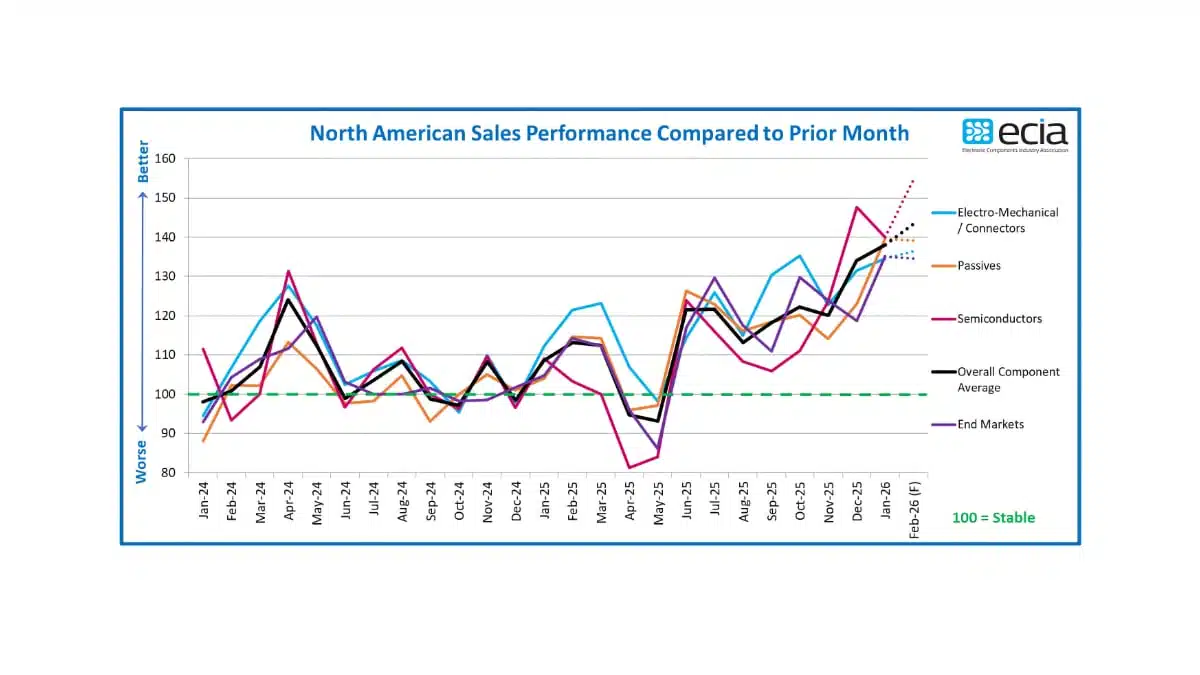

The overall average index score for electronic component sales sentiment reached 138.0 in January 2026 and is projected to rise further to 143.4 in February. This marks the eighth consecutive month with the total index above 110, clearly above the neutral threshold of 100 that separates positive from negative sentiment. Only the March through May 2021 period produced stronger readings in the survey’s history.

Industry participants across the authorized supply chain report a notably positive self‑assessment as 2026 begins. The consistently elevated sentiment suggests that recent improvements are not short‑lived, but rather part of an extended upswing in demand and confidence.

Segment Highlights – Semiconductors, Passives, and Electro‑Mechanical

Despite a modest decline of 7.6 index points from December to January, the Semiconductor category remained the strongest of the three major product segments with a score of 140.0. Passive components recorded a sharp 16.7‑point month‑over‑month surge to 139.6, nearly closing the gap to Semiconductors. Electro‑Mechanical and Connectors achieved a solid score of 134.5, reflecting a modest but meaningful improvement.

Looking ahead to February, survey participants expect the Electro‑Mechanical and Passive components categories to maintain their strong sales sentiment with only minor adjustments. Semiconductors, in contrast, are projected to exhibit an exceptional jump in strength, with the segment’s overall index forecast to leap to 154.5. Within Semiconductors, Memory ICs stand out with record‑breaking scores of 180 for both January and the February outlook, indicating exceptionally strong demand.

While MCU and MPU devices and Analog or Linear ICs are comparatively weaker within the semiconductor space, their index scores still fall between 120 and 140. This places them well within positive territory and confirms that momentum is broadly distributed, even among the less heated sub‑segments.

End‑Market Outlook – Broad‑Based Demand Strength

End‑market sentiment improved significantly in January, bringing it into alignment with the strong product category scores. The overall end‑market index reached 135.1 in January and is expected to remain relatively stable into February, indicating that customers across application areas share the positive outlook.

Every tracked end‑market segment posted index scores above 100 for both January and the February forecast. Optimism is particularly strong in Avionics, Military, and Space, as well as Industrial applications, where ongoing programs and investment cycles continue to support elevated demand. The combination of strong product and end‑market readings reinforces the view that the current strength is not confined to a narrow set of applications.

Supply Chain Sentiment Across Channel Partners

All major supply chain participant groups reported firmly positive sentiment in January and for the February outlook. Manufacturer Representatives recorded the strongest sales sentiment scores, followed by Distributors. Manufacturers, while more conservative in their assessments, still reported solidly positive results across all categories.

Notably, every product and channel combination achieved index scores at or above 100 in both January and the early‑2026 outlook. This across‑the‑board alignment suggests a high level of confidence and consistency among different parts of the authorized supply chain, from production through to the sales interface with end customers.

Rising Lead Time Pressure and Memory Supply Concerns

Alongside the strong demand outlook, lead time pressures are increasing, particularly for Semiconductors. More than half of survey participants report longer lead times for semiconductor devices, and nearly 40% of all respondents see lead times increasing across the board, compared to only 8% who report shortening lead times.

Advanced memory ICs are under the greatest strain. DRAM and NAND Flash show especially acute pressure, with 75% and 67% of respondents respectively reporting increasing lead times for these devices. The acute mismatch between supply and demand for advanced memory ICs is emerging as a major concern for the health of the broader electronics components market.

Tight availability of these critical components poses a risk of stalled or delayed sales in other product segments and end‑markets that depend on them. As the industry moves further into 2026, managing memory IC supply has become one of the most critical priorities in supply chain planning and risk mitigation.

Source

This article is based on information and data provided in an ECIA Industry Pulse and ECST report press release prepared by ECIA’s chief analyst and the association’s research team.