The German component distribution market returned to solid growth in Q1 2026, driven by strong order intake and a sharp rebound in semiconductors and IP&E, but framed by rising AI‑driven memory prices and renewed supply chain risks.

Market snapshot: Q1 2026

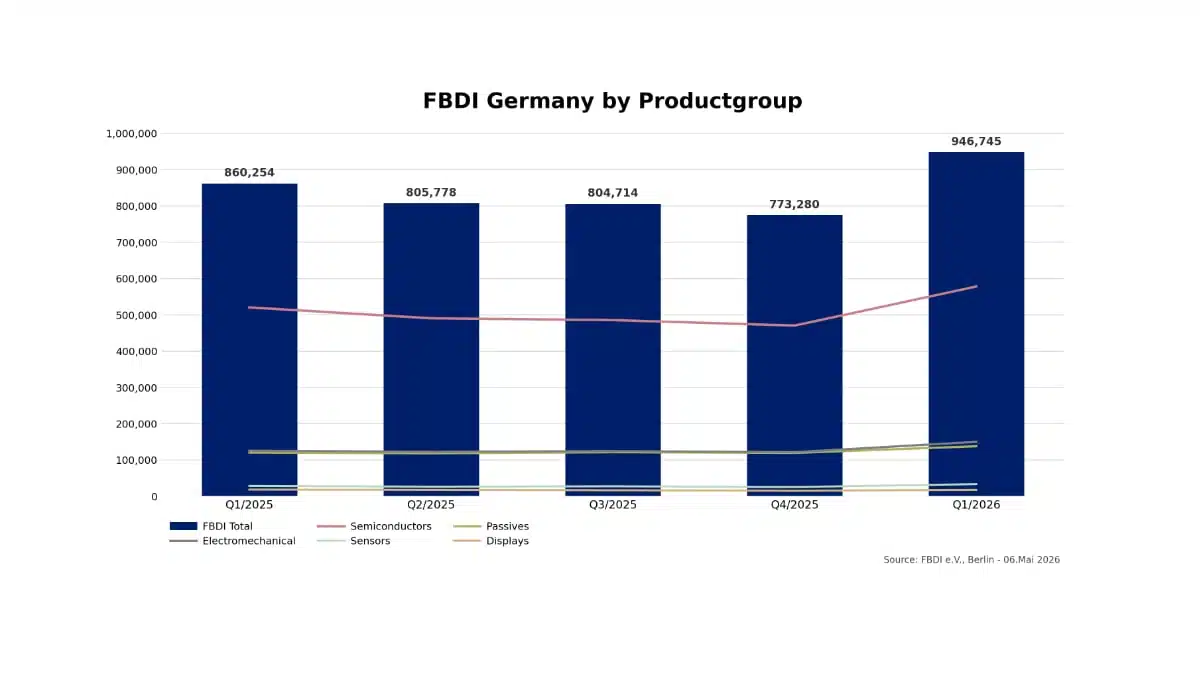

The German electronics distribution market achieved sales growth of 10.1% versus Q1 2025, with a book‑to‑bill ratio of 1.44 signaling sustained recovery rather than a short‑term spike. Incoming orders jumped by 63.7%, pointing to renewed project activity and a clear normalization from the downturn phase of 2023–2024. At the same time, the global environment remains tense, with capacity concerns, fragile supply chains, and a worldwide semiconductor market that expanded by 61.8% year‑on‑year in February 2026 according to WSTS.

Price surges in the memory segment are feeding directly into the German market and creating distortions between product groups. Distributors and OEMs are increasingly confronted with the challenge of balancing real demand against speculative and price‑driven booking patterns.

Between industrial strength and AI dynamics

Structural positioning of Europe

The German and broader European electronics markets remain more closely linked to industrial applications than to the AI hyperscale cycles that dominate demand in the US and Asia. This industrial orientation makes the market development more consistent, with fewer extreme peaks, but still vulnerable to external shocks such as geopolitical crises and energy market volatility.

According to FBDi Managing Director Andreas Falke, the positive trend from late 2025 has clearly continued into Q1 2026, driven by stable pricing and a visible recovery in demand, while concerns over availability and logistics are once again increasing. Global instability and regional conflicts add uncertainty but have not yet undermined the underlying growth potential of the German electronics industry.

Product group development

Semiconductors: strong but highly volatile

Semiconductors remained the dominant growth engine, but with pronounced volatility across sub‑segments. In Q1 2026, semiconductor revenues reached 577.6 million euros, representing growth of 8.4% year‑on‑year. The overall semiconductor book‑to‑bill ratio stood at 1.62, clearly in expansion territory.

The memory segment was the standout driver, with revenues surging by 115.8% and incoming orders increasing by around 590%, pushing the book‑to‑bill ratio for memory to 3.42 and setting new historic highs. This movement is directly linked to global AI investments, which are creating capacity bottlenecks and massive price increases in memory and parts of the logic segment. For the German distribution channel, this translates into exceptionally strong bookings, but also into the risk of future corrections once capacity and pricing normalize.

Optoelectronics, MOS Micro, PLD: ordering boom with distortions

Optoelectronics, MOS microcontrollers, and programmable logic also recorded substantial rises in incoming orders, each with growth rates of more than 60%. This demand surge reflects both AI‑adjacent applications and broader digitalization and automation projects in industrial and infrastructure markets.

However, the momentum is double‑edged: alongside genuine demand, strategic stockpiling and price expectations are clearly influencing order behavior. This creates the potential for pronounced market distortions in the coming quarters, with both upside and downside scenarios possible, depending on whether bookings are matched by real end‑customer consumption. It also remains open whether these dynamics will spill over into other product groups or instead act as a brake on broader market development.

IP&E: stable backbone of the market

The IP&E segments (interconnect, passive and electromechanical components) presented a much more stable and less volatile picture in Q1 2026. Total IP&E revenues reached 320.7 million euros, equivalent to 11.8% growth versus the prior year quarter, with a book‑to‑bill ratio of 1.17.

Passive components contributed 137.4 million euros in revenue, also up 11.8%, supported by robust industrial demand and a 28.1% increase in incoming orders. Electromechanics remained a reliable pillar of growth, with revenues of 149.6 million euros (+14.8%), a book‑to‑bill ratio of 1.22, and incoming orders up by 33.4%. These segments are closely linked to automation, energy infrastructure, and building technologies and therefore benefit from long‑term transformation trends rather than purely speculative AI cycles. Overall, IP&E shows broad‑based, sustainable growth that is strongly rooted in real industrial applications.

Outlook: opportunities and risks for 2026

Growth base and structural tailwinds

The strong order intake in Q1 2026, combined with the recovery already visible in the second half of 2025, forms a solid starting point for the current year. Growth impulses are emerging in particular from AI infrastructure build‑outs, defense and aerospace programs, the energy and mobility transition, and advanced system integration. Long‑life industrial applications, for which Europe and Germany are key hubs, remain an important stability factor along the electronics value chain.

At the same time, the market faces significant risks: geopolitical tensions, ongoing supply chain fragility, the concentration of AI‑driven demand in other regions, and increasing requirements around energy and raw material security. From FBDi’s perspective, Europe now needs clarity, courage, and shared priorities to leverage its industrial strength and transform the current momentum into a more resilient and globally competitive position.

Source

This article is based on information and data provided by the FBDi e.V. press release on the German component distribution market in the first quarter of 2026, supplemented by the association’s own market assessment.